Still confused about

those sizzling new economic-growth figures coming out of India? You’re not alone.

The country’s Central Statistical Office invited analysts and economists to a daylong workshop in New Delhi this week, hoping to explain and clarify the

recent revisions to its methodology for estimating gross domestic product.

Those revisions suddenly caused

India’s projected growth rate to shoot past China’s, which in turn thrust the nuts and bolts of India’s GDP calculation into the spotlight. Officials were pelted with questions as they walked through the new data sources, the updated surveys, the tweaked methods of extrapolating and scaling and counting.

Much of the information about the new GDP method had already been made public in a

144-page document released last month. But who has the time? Here are some highlights.

1. In India, all cars used to be equal. In earlier Indian GDP data, the key manufacturing indicator was the monthly index of industrial production, which is based on the total quantity of output in a sample of a few thousand factories.

“The problem is that Marutis and Audis are all put together as the same,” said Ashish Kumar, director-general of the Central Statistical Office. In other words, by gauging only the volume of production, the old series was overlooking changes in monetary value brought about by product improvement and differentiation.

In the old GDP series, a yearly survey of industrial firms supplemented the production index when it became available. But that survey, too, has a limitation: Because it measures activity at the factory level, it doesn’t account for the marketing, development, logistics and financial-planning activities that take place at manufacturing firms’ head offices.

“In the earlier series, we were not capturing this,” Mr. Kumar said. “Because we never had access to any such information.”

The new GDP series therefore incorporates a new database of company balance sheets from the Ministry of Corporate Affairs. For the year ended March 2012, the database includes information from more than 500,000 firms. A central-bank study that had been used previously to gauge corporate activity covered fewer than 2,500 companies.

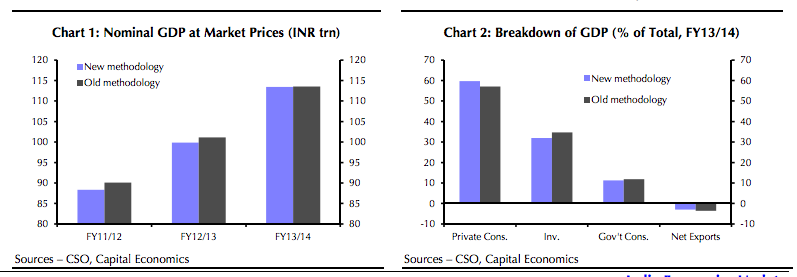

The impact on final growth rates is huge—and still slightly hard to swallow. In the 12 months that ended March 2013, manufacturing expanded 6.2% in the new GDP series, compared with 1.1% in the old. And in the following year, for which the old series had shown a 0.7% contraction, the new series has manufacturing growing by 5.3%.

2. All workers used to be equal, too. Well, at least for gauging activity in the informal economy. Small, unregistered companies—a major chunk of the Indian economy—typically employ unpaid helpers in addition to owners and hired workers. But before, these firms’ output was being estimated by taking the total number of workers and multiplying by per-capita added value.

No longer. The new GDP series uses an “effective labor input” method, which assigns different weights to different kinds of workers based on their productivity. The chart is here:

Central Statistical Office

3. Agriculture isn’t just about crops, and livestock isn’t just about meat. Two major changes in the agricultural component of the new GDP series have to do with livestock. The first is a new way of valuing “meat byproducts.” State governments had been failing to provide direct data on the values and quantities of animals’ heads, legs, fat and skin on a “systematic and regular basis.” So, thanks to a study by the

National Research Center on Meat, in Hyderabad, these are now being recorded simply as a share of the total value of the animals’ flesh.

Here’s the chart:

Central Statistical Office

Yum. “EOG” stands for “edible offals and glands.”

The second major change to livestock measurement has to do with a different kind of byproduct. “For the first time, we have included the evacuation rate of goats and sheep in the production of organic manure,” said Sunil Jain, a deputy director-general at the statistics office.

Translation: Using a study on how much those animals defecate, statisticians have added that particular kind of biological output to their economic value.

The estimated “evacuation rates” are 0.3 kilograms per day for goats and 0.8 kilograms per day for sheep. The study, titled

“Positive Environmental Externalities of Livestock in Mixed Farming Systems of India,” was conducted jointly by the

Central Institute for Research on Goats, in Makhdoom, Uttar Pradesh, and the

National Center for Agricultural Economics and Policy Research in New Delhi.

With all those “droplets” added in, the value of India’s livestock sector in the new GDP series is 9.1 billion rupees, or $150 million, higher than it was in the old series.

Why did the Central Statistical Office choose to start counting droplets? “It is based upon the observation of the farmers that, ‘OK, if I have to increase the fertility of my soil, I would request a shepherd to leave many animals in my field for a week,’ ” Mr. Jain said.

4. Finance is still a pretty new industry in India. Or at least measuring the financial industry is pretty new.

In the previous GDP series, the industry had two main components: banking, which made up 80.1% of added value in the sector, and insurance, which made up the rest. In fact, in the official guide to the old GDP figures, the financial industry was called just that: “Banking and Insurance.”

By contrast, the new GDP series includes separate measurements of stock exchanges and stock brokers. It counts the growing plethora of private investment funds available to Indians. In the old GDP figures, UTI, the formerly government-managed investment vehicle, had been the sole mutual or money-market fund being measured. The Employees’ Provident Fund Organization, the state-run social-security program, was the only pension fund.

Not even informal finance,

hardly a recent scourge in poorer corners of India, was being estimated separately before the latest GDP series. It was just assumed to be one-third the size of the formal, non-bank financial industry. Now, private moneylenders’ contribution to the economy is measured using survey data from the central bank.

5. Hoarding gold is now officially virtuous. In the new GDP series, households’ expenditure on gold and silver ornaments is treated as part of their savings instead of their consumption. The value of such savings, in the year ended March 2012, was recorded at 340 billion rupees, or $5.4 billion—which, despite Indians’ infamous appetite for gold, represented only 1% of total savings in the economy that year.

6. When it comes to timely economic data, India is still far, far behind rich countries.The biggest obstacle to measuring the Indian economy is how much of it is informal: cash-based, outside the tax net and leaving no paper trail. Two-thirds of India’s nonfarm workforce are employed this way.

With measurements on such a large portion of the economy available only via surveys conducted once every five years—less often in some cases—Indian statisticians invariably rely on various workarounds to produce yearly GDP numbers. For the informal economy, the new series uses tax and corporate data instead of blunter indexes of production to project survey findings forward.

That’s ostensibly an improvement. But India’s data deficiencies don’t end there.

In rich countries, GDP can be triangulated: Whether you tally up the value of what’s produced, the money that is spent to buy that production or the income earned from selling it, the total should be the same. Not so in India, where only production data are considered reliable.

Data on securities and other financial instruments are underdeveloped as well. India doesn’t have regular statistics on employment.

“There’s a large number of areas where we have deviated” from the United Nations’ latest guidebook on measuring GDP, said T.C.A. Anant, who holds the title of chief statistician of India—“for a large measure, because we are simply, at the moment, unable to implement those recommendations.”

India’s New GDP Numbers: A Peek Under the Hood - India Real Time - WSJ

India’s Finance Mnister Arun Jaitley forecast exactly a month ago that the country’s GDP growth rate will be 7.5 percent this year. He attributed this entirely to the dynamism of the government led by Prime Minister Narendra Modi formed after the 2014 parliamentary poll. “During the last few years we had fallen off the radar, our growth had slowed down, our priorities were blurred and the world was accusing us of policy paralysis. Finally people of India decided to bring about a change”, Jaitley said in a thinly veiled condemnation of the previous government led by Prime Minister Manmohan Singh, an acclaimed economist himself, who is credited with piloting the country’s free-market reforms.

“This year we will close at 7.5 percent GDP growth and next year hopefully higher,” Jaitley predicted. Jaitley is a no-nonsense lawyer by profession and is a successful politician. To be sure, as India’s finance minister, his words carry weight within the country and abroad.

They influence even the IMF, which has since acclaimed that India is poised to “overtake” China in growth. That’s a tongue-in-cheek remark, of course, because who doesn’t know that China’s economy has outstripped India’s by four decades or more already and comparing India with China is no more than a folk tale. But then, perceptions form the stuff of our day-to-day life and most of us Indians are not trained economists.

Unsurprisingly, the widespread perception in India today is that the country has finally caught up with China in growth and development. For a country smitten by a keen sense of envy bordering on rivalry vis-a-vis China, this easily transmutes as the stuff of national pride. And Prime Minister Narendra Modi suddenly looks ten feet tall.

Even President Barack Obama took note, which was only to be expected since the lure of the fastest growing market in the world is there on his mind always. The Indian market is important for boosting US exports and creating jobs in America and it could not have escaped Obama’s highly focused mind.

Obama probably thought it will be a clever move on his part to pen a panegyric on Modi. There couldn’t be a better way of flattering Modi, after all. And, believe it or not, amidst all that ugly, exasperating wrangle with the US Congress over the Iran deal, Obama was quietly writing a panegyric on Modi!

But nothing works well for Obama thse days and the Time magazine’s piece by the US president on Modi, which appeared yesterday, however, turned out to an overkill that might even embarrass Modi, who usually likes flattery.

Obama probably thought it pays to cater to Modi’s vanities, since he knows Modi can take arbitrary decisions and that can be useful for promoting American business interests. But he stepped way out of line by bracketing Modi with Martin Luther King and Mahatma Gandhi. The point is, like what the famous song supposedly about Sophia Loren says, Obama never looked inside Modi’s head.

Obama’s panegyric most certainly inspired Jaitley to exceed his own month-old prophecy. He now believes that India has the potential to make nine to 10 percent growth rate “a new normal.” He made this prophecy at a US-India business conclave organized by a Washington-based think tank.

If Obama gets to hear what Jaitley just announced, maybe, he will now do an oil painting of Modi. Anything is possible. Obama has a focused mind.

To be sure, Jaitley has proved to be a past master in the ancient Indian rope trick. He has done a masterly job in stringing the public opinion and duping Obama by creating the misperception that under Modi’s magical touch, Indian economy has turned the corner and is zipping ahead.

How India bettered China’s growth story | Asia Times