June 17, 2014

Smart City Development in China

Officials are turning to technology to improve efficiency and tackle problems in urban China.

By Don Johnson

The next time you visit Zhenjiang, Jiangsu, don’t forget to visit the app store first. In this historic Yangtze River city near Suzhou, you can check the arrival time of the next bus, make an appointment at a city hospital, and find parking spaces or public bicycles—all from your smartphone.

Zhenjiang city buses continuously report their position and operating characteristics to a “smart dispatch” control center, helping operators improve scheduling efficiency and reducing fuel use and emissions. In a pilot project, some buses are now also sporting fast 4G wireless internet for riders. According to the city, half a million riders a day are checking bus arrival times using smartphone apps, and the city is saving 6,700 tons of carbon dioxide and ¥17 million ($2.7 million) in fuel costs per year.

Although it was an early adopter, Zhenjiang is far from the only city in China trying to improve efficiency and service through technology. The central government has made development of smart city technology and projects a key national policy, and it’s now difficult to find a Chinese city of any size that does not have aspirations to be “smart.” With millions of rural migrants arriving every year and environmental and economic pressures mounting, Chinese cities can surely use all the smart they can get. But are smart city projects really a solution—or just the latest policy buzzword?

The 2010 Shanghai Expo was an early test of many smart city technologies in China, as well as an important promoter of the smart city concept. (Photo by Donald Johnson)

What is a smart city?

“Smart City” is a slippery term applied to everything from urban design to higher education policy. But the most accepted definition is the use of information technology to attack urban problems. Database and network systems developed in Silicon Valley to power Google, Amazon and Facebook—not to mention Taobao and WeChat—are now being connected to objects in the physical world such as meters, sensors, cameras, and control systems in pilot projects around the world. Smart city systems are managing traffic, stabilizing electric grids, allocating and coordinating emergency services, and providing more city information to people and managers than has ever been available before.

To date these systems have mostly been installed independently of each other. But multinational companies, including several from China, are now in a race to develop and deploy smart city platforms in which disparate systems communicate and share information. For example, if a sudden rainstorm flooded storm sewers in an area, sensors and social media traffic could quickly alert managers, who could then issue public announcements (again using social media), reroute traffic and public buses, and dispatch workers to resolve the problem. The leading example of this kind of connected and data-driven urban management is Rio de Janeiro’s Operations Center, set up by IBM in 2010. It coordinates information from 30 municipal and state agencies, and

can manage traffic control and emergencies in real time. When three buildings collapsed in 2012, the operations center coordinated dispatching emergency personnel, closing nearby metro stops, and rerouting traffic.

More ominously, such systems offer an unprecedented level of surveillance and control of public spaces, and a means to assemble a tremendous amount of data on individual citizens. Worldwide, cities are still in the early stages of understanding and managing the capabilities these systems can provide, and smart city technology companies have also not been as proactive as they could be in addressing privacy and data security issues. In China, there has been little or no public discussion of this facet of the smart city vision, and some international companies, such as Cisco, have been

criticized in their home markets for supplying China with surveillance technology.

For Chinese leaders, smart city technology looks like a win-win. For several decades, 20 million peasants a year have moved from the countryside to urban factories and construction sites, fueling China’s legendary economic rise. This immense migration is far from reaching an end: China is currently only half urban, less than other mid-level developing countries such as Malaysia (73 percent urban) or developed nations like the United States (80 percent), and the Chinese government is counting on further urbanization to support economic development. What is now worrying Beijing is whether cities can support an additional 100 million residents. Pollution, housing affordability, and traffic congestion are already taking a heavy toll, so policy-makers are looking urgently for ways to let cities continue to offer migrants a better life. At the same time, economic planners are pushing hard to transform China from the world’s export factory to a self-sufficient modern service economy, and smart city technology looks like a good investment.

Cities with smart city projects at the end of 2013, according to CCID Consulting. (Source: Donald Johnson/CCID Consulting)

A big bet on smart cities

This is the backdrop for China’s large and sustained bet on smart city projects. The 12thFive-Year Plan, which guides broad economic policy through 2015, specifically calls out smart city technology as a sector to be strengthened and encouraged, and ministries are jostling to sponsor programs and industry alliances. In 2012, the Ministry of Science and Technology (MOST) organized the China Strategic Alliance of Smart City Industrial Technology Innovation. Last year, the Ministry of Industry and Information Technology (MIIT) sponsored another group, the China Smart City Industry Alliance, and this year announced a ¥50 billion ($8 billion) fund to invest in smart city research and projects. A third group, the Smart City Development Alliance, was formed this spring by the National Development and Reform Commission (NDRC). Some companies are working with only one of these new groups, and some are involved with all three. At present there is little connection between the groups, which apparently exist to improve communications between industry participants and between industry and government and, in the case of at least the MIIT group, to coordinate investment.

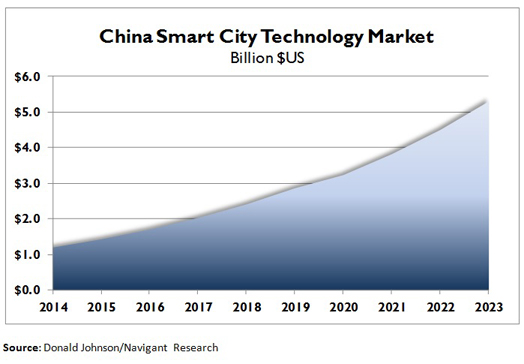

The most far reaching effort, however, is led by the Ministry of Housing and Urban and Rural Development (MOHURD). Last year, MOHURD selected 193 local governments and economic development zones as official smart city pilot project sites, making them eligible for funding from a ¥100 billion ($16 billion) investment fund sponsored by the official China Development Bank. Investment from local government and private sources has also been growing fast: There’s no standard definition of the sector, but some estimates foresee ¥2 trillion ($320 billion) of investment into smart city development projects over the next 10 years. A more focused projection that I did for Navigant Research at the end of last year, looking only at the “smart” technology component in smart city projects, anticipated a cumulative market of $28.5 billion ($4.6 billion) over the next 10 years in mainland China, Hong Kong, and Taiwan. Defined broadly or narrowly, the investment will be huge.

These enormous sums, rapid technology advances, and vigorous marketing of smart city products from both domestic and international companies, have created a booming and chaotic marketplace. Both boosters and critics of smart cities are now concerned that local governments eager to juice their economies will see this indiscriminate encouragement as a blank check. In Beijing the effort now is to create standards and guidelines to manage this flood of new projects. This spring, all the ministries involved joined with the Standardization Administration of China to create working groups whose job is to manage and standardize smart city development, though their activities have not been publicized.

The private sector: smart city suppliers

The private sector: smart city suppliers

The smart city sector is not a single industry, but an emerging collection of technologies cutting across many industries – transportation and utility infrastructure, network equipment, telecom and wireless, data analytics, electronics equipment, and software applications. To manage the torrent of information, applications rely heavily on new IT technologies such as cloud computing and “big data” analytics. Some companies—IBM and Cisco, for example—have made the smart city concept a centerpiece of their marketing efforts around the world, although no firm covers the entire industry chain. Currently, many disparate companies are extending their reach through partnerships and acquisitions. This has created alliances that would once have seemed incongruous. For instance, utility meter manufacturer Itron has teamed up with Microsoft to create a management app for Windows.

For international companies, huge opportunities in China are tempered by real challenges. The local government market is famously opaque, and smart city applications sometimes involve areas – digital mapping, for example – considered sensitive for non-Chinese firms. US firms in particular face increased scrutiny in the wake of the Congressional investigation of Huawei, the revelations of global NSA surveillance from whistle-blower Edward Snowden, and the US Justice Department’s recent move to name five members of the Chinese military to its most-wanted list for cyber-attacks against US companies. This last move has provoked several countermeasures from China, including the

banning of Microsoft’s Windows 8 from government offices and the reported

phasing out of IBM servers from Chinese banks. The recent announcement from the State Information Office that it would be testing the security (as yet undefined) of foreign information technology products and services, and barring those that do not pass, only further underscores the difficulties that international firms may face in China.

But the most significant challenge may be China’s rapidly maturing domestic competition. China is no longer a developing-nation market in which international companies compete only with one another. In typical fashion, Chinese firms have been adept at mastering technologies and shaking up markets, often by offering low prices. Huawei, for example, in

2012 assumed the title of world’s largest telecommunications equipment manufacturer, previously held by Ericsson. Telecom equipment manufacturer ZTE and integrated IT firm Digital China compete directly against international firms such as Ericsson and Oracle. And a host of smaller firms, primarily manufacturers and software application providers, are targeting the smart city market.

The situation is somewhat different for infrastructure-based providers like Siemens and Schneider Electric; their competitors tend to be state-owned, and large infrastructure projects often end up as collaborations between local and international firms. China’s two electric grid companies, State Grid and Southern Grid, as well as all three of its major telecoms, are actively developing smart grid policies and products and sponsoring pilot projects.

Yet with their strengths in technology, quality, and brand, international firms continue to expand. Their involvement in the development of smart city projects globally gives them a strong advantage that may not last, as Chinese firms move aggressively into developing markets elsewhere in Southeast Asia, India, Africa and Latin America—and occasionally into developed markets as well.

In China, there are many stand-alone projects based on a few core applications such as energy, transportation and government management platforms, but even at the pilot level there are not yet any comprehensive smart cities. But China has committed to its cities and is placing large hopes on technology to make them manageable and livable. The plans being prepared and submitted to MOHURD by nearly 200 demonstration sites have not been made public yet, but it will be surprising if there are not some groundbreaking projects among them. It’s not an exaggeration to say that the success of China’s smart city investment is one of the key conditions for the country’s continuing long-term prosperity.

ABOUT THE AUTHOR

Don Johnson (

djohnson@ddj-consulting.com)is an urban planner, economist, and the principal of DDJ Consulting (

DDJ Consulting | Urbanization, Urbanism and Technology in China Based in Shanghai, he has been leading planning and research projects across China for over seven years. He is the author of Navigant Research’s “Smart Cities: Asia Pacific,” released this March, and has contributed to smart city development projects both inside and outside China.

(Photo by Ol.v!er [H2vPk] via Flickr)

Smart City Development in China | China Business Review