Not just any dictator, one capable of Alchemy.Hopefully the Pakistani Military installs a dictator before the country totally collapses.

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Is Pakistan poised for default in FY 2024?

- Thread starter ghazi52

- Start date

Pakistan's problems aren't actually that hard to fix.Not just any dictator, one capable of Alchemy.

The civilian leadership simply doesn't have any incentive to fix them.

Tamerlane

FULL MEMBER

- Joined

- May 30, 2012

- Messages

- 1,304

- Reaction score

- 3

- Country

- Location

Pakistan was only balancing relations between the US and China as long as US-Chinese relations were good. As soon as the US decided to go into confrontation mode with China Pakistan has started siding with the US.

The generals have clung to the UK/US since the British left. They have their families and money in the West. Their retirement plans are in the West. Their weapon systems are from the West. Even most trade is with the West.

Knowing full well for decades that the US is not a reliable supplier of defense equipment the generals have made little effort to move away. Bajwa even admitted that they only buy Chinese weapons if the US refuses.

So, they’ve got no choice but to side with the US if forced to choose between it and China. The US knows that, so they don’t even bother to compete for Pakistan’s friendship.

India is buying defense equipment from both the US and Russia. America is trying to bribe India with massive investment and a strategic partnership. They’re installing Indians in high positions. India is milking them for everything it can get and still working closely with Russia.

Meanwhile Pakistan gets nothing. No investment, no IMF loans. The Americans don’t even have to pay bribes to the generals. The generals steal all the money they want from Pakistan and transfer it to America. All America had to do is look the other way and issue some green cards.

A few visas for the generals is all it takes to buy Pakistan.

The generals have clung to the UK/US since the British left. They have their families and money in the West. Their retirement plans are in the West. Their weapon systems are from the West. Even most trade is with the West.

Knowing full well for decades that the US is not a reliable supplier of defense equipment the generals have made little effort to move away. Bajwa even admitted that they only buy Chinese weapons if the US refuses.

So, they’ve got no choice but to side with the US if forced to choose between it and China. The US knows that, so they don’t even bother to compete for Pakistan’s friendship.

India is buying defense equipment from both the US and Russia. America is trying to bribe India with massive investment and a strategic partnership. They’re installing Indians in high positions. India is milking them for everything it can get and still working closely with Russia.

Meanwhile Pakistan gets nothing. No investment, no IMF loans. The Americans don’t even have to pay bribes to the generals. The generals steal all the money they want from Pakistan and transfer it to America. All America had to do is look the other way and issue some green cards.

A few visas for the generals is all it takes to buy Pakistan.

Redbeanpaste

FULL MEMBER

- Joined

- Jun 6, 2020

- Messages

- 272

- Reaction score

- 0

- Country

- Location

Why? Doesn't China have a relationship with the US?pakistan will have to make a choice soon

Do we ask them to make a choice?

Having said that ...we can't get rich ...or even just stop being dirt poor without daddy America.

Most of our exports are to the west

Most of our imports are from China

That says something

PradoTLC

ELITE MEMBER

- Joined

- Mar 17, 2007

- Messages

- 8,878

- Reaction score

- -3

- Country

- Location

.,.,.,

Is Pakistan poised for default in FY24?

Khurram Husain

June 14, 2023

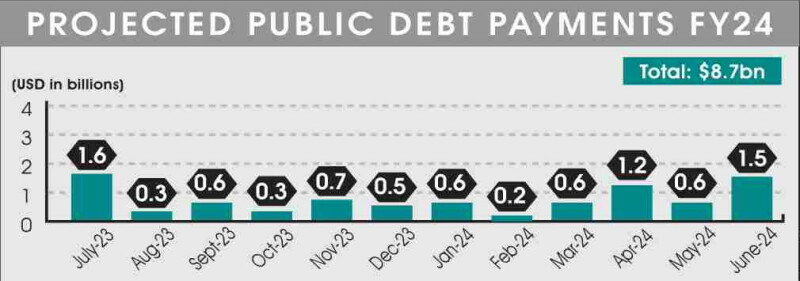

WITH dangerously low foreign exchange reserves and a steep debt repayment schedule looming for fiscal year 2024 that begins in July, Pakistan is facing a stark prospect of potential default or even a larger balance of payments crisis in the 12 months ahead.

Data obtained unofficially from a senior source privy to the country’s debt repayment schedule shows Pakistan faces $8.7 billion outflows on public debt payments in FY24 (including principal and interest) that are not subject to rollover.

On top of this, there is another $5bn approximately on private debt outflows as per the IMF staff report released in September 2022, bringing the total to $13.7bn in debt-related payments. Repayments on account of publicly guaranteed debt are on top of this.

The monthly schedule of outflows as per this government data is shown in the attached graphic. Assuming zero current account deficit, all rollovers going smoothly, debt payments made on time and no external financing support, the data shows State Bank’s foreign exchange reserves going negative by December of this year.

A large payment of $1.6bn is due in July, including $1bn of a Chinese SAFE deposit that is maturing and has been rolled over smoothly in all years since it was drawn. Government accounting convention requires it be listed as an outflow until a rollover date has been agreed between both parties. Should it be rolled over successfully again this year, July will still see a sizable outflow of $600 million.

June is already seeing hectic activity around debt repayments. In an analyst briefing following Monday’s monetary policy decision, the State Bank governor said $3.6bn was maturing this month, of which $400m has already been paid and another $2.3bn is likely to be rolled over.

“We have concurrence from both sides on this,” he told the attendees, though it seems a date has not yet been agreed because the amount is still being counted as an outflow. That still leaves a $900m further debt service bill in June to be covered from the reserves that are below $4bn already.

Of the total outflows on public debt account scheduled for the next fiscal year, $4.7bn is in July to December. April 2024 sees a large bond maturity when outflows leap to $1.2bn, and June 2024 sees another $1.5bn maturity of several instruments, only some of which are eligible for rollover.

If the government succeeds in the next few days in getting a rollover on the $2.3bn loan from a consortium of Chinese banks that was announced on June 22 last year, the scheduled outflow for June 2024 will rise to $3.8bn since these maturities will then fall due next June.

According to the last IMF staff report, private debt repayments on external account for FY24 are $5bn. These funds are also, under normal circumstances, rolled over fairly easily provided the borrower has been servicing the loan on time. Whether or not they’ll represent a drain on the reserves in the forthcoming year depends on the ability of these borrowers to continue servicing their loans in foreign exchange.

The same report shows Pakistan’s total public debt repayments to be just under $20bn, with another $1.68bn to be repaid to the IMF, and $13bn given as rollover on short-term debt. These numbers suggest outflows on public debt payments should be $8.7bn, consistent with unofficial government figures obtained by Dawn.

But this figure differs greatly from other numbers compiled by sovereign debt advisory firms and private creditors who hold Pakistani bonds. One such data panel, drawn up by a European firm and seen by Dawn, shows public external debt servicing for FY24 to be slightly higher than $14bn.

These creditors and firms triangulate their numbers from various sources, including databases maintained by Bloomberg, the World Bank and the IMF. When Dawn asked one of them for an explanation as to why their estimate for Pakistan’s debt service obligations for FY24 differs so widely from the one provided by the government, they offered various theories but were unable to reconcile the difference mainly because they could not agree on the assumptions that went into deciding which debt obligations will be rolled over and which ones will not.

“We never used this figure,” one individual, who has worked on estimating Pakistan’s debt service obligations, said, referring to the $8.7bn number. The person did not wish to be identified due to the sensitivity of the matter. “Because we never managed to understand what they assume will be rolled over.”

According to these individuals from the private sector, the $13bn assumed to be rolled over in FY24 seems too large. “I understand that this would include $7bn of SAFE and Saudi deposit, maybe $1bn of Islamic Development Bank facility. But I am having a hard time understanding where the other $5bn of rollovers come from,” he continued.

Complicating matters further, budget documents show repayment of foreign and short-term credits as $15.3bn in FY24. Against this figure, they show total external inflows to be $24bn, including $4.5bn in commercial borrowing, $4bn in a new SAFE deposit from China, $6bn deposits from Saudi Arabia and the United Arab Emirates and a $1.5bn international bond. How many of these inflows will actually materialise is another large question mark.

Whichever figure one takes — $8.7bn or $14bn or $15.3 — one thing is clear: there is no clear financing plan to meet these obligations for next year.

The government is projecting a current account deficit of $6bn. Coupled with the debt service payments, each of these figures yields an external financing requirement of either $14.7bn or $20bn or $21.3bn.

The plan chalked out by the government sounds optimistic in the absence of an IMF programme. And Finance Minister Ishaq Dar could have complicated the government’s efforts to secure the critical rollovers looming in June and July this year with his premature talk of a possible “debt restructuring”.

Seen from any angle, FY24 is going to see serious headwinds for the external sector, with ramifications for the exchange rate, inflation, and possibly even the integrity of the energy supply chain should the forex shortages intensify.

The country started FY23 with SBP reserves of $9.7bn. It made debt service payments of $9.7bn from July to April, and secured debt-creating inflows of $7.3bn in the same period, yielding a net drain of $2.4bn on the reserves. Coupled with a current account deficit of $3.3bn, the reserves fell by $5.7bn in this period.

No major covenants have been broken with the country’s external creditors so far. But for the next fiscal year Pakistan is looking at a higher debt service bill, very slim chance of securing further external financing support, and far lower level of reserves than last year.

The possibility of landing up in a situation where the foreign exchange reserves can no longer support even the basic life support systems of the economy is now a clear and present danger. If financing support does not arrive fast, the situation would have lingered too close to the edge for too long for a country of 220 million people.

Situationer: Is Pakistan poised for default in FY24?

Data shows State Bank’s foreign exchange reserves going negative by December of this year.www.dawn.com

All lies …

$ Darr has confirmed Pakistan will not default …

Pakistan was only balancing relations between the US and China as long as US-Chinese relations were good. As soon as the US decided to go into confrontation mode with China Pakistan has started siding with the US.

The generals have clung to the UK/US since the British left. They have their families and money in the West. Their retirement plans are in the West. Their weapon systems are from the West. Even most trade is with the West.

Knowing full well for decades that the US is not a reliable supplier of defense equipment the generals have made little effort to move away. Bajwa even admitted that they only buy Chinese weapons if the US refuses.

So, they’ve got no choice but to side with the US if forced to choose between it and China. The US knows that, so they don’t even bother to compete for Pakistan’s friendship.

India is buying defense equipment from both the US and Russia. America is trying to bribe India with massive investment and a strategic partnership. They’re installing Indians in high positions. India is milking them for everything it can get and still working closely with Russia.

Meanwhile Pakistan gets nothing. No investment, no IMF loans. The Americans don’t even have to pay bribes to the generals. The generals steal all the money they want from Pakistan and transfer it to America. All America had to do is look the other way and issue some green cards.

A few visas for the generals is all it takes to buy Pakistan.

I know we are so cheap … we sell our selves for Pennies

WarKa DaNG

SENIOR MEMBER

- Joined

- Aug 26, 2014

- Messages

- 2,446

- Reaction score

- 0

- Country

- Location

Can somebody tell me where is that economic expert who said that dollar got cheaper and stock exchange performed better with the arrival of the buffoons

The current civilian leadership is way better than Imran Khan, but are still not enough to overcome the accumulated problems from civilian rule.Can somebody tell me where is that economic expert who said that dollar got cheaper and stock exchange performed better with the arrival of the buffoons

Pakistanis are incapable of ruling themselves, and only a military government has any chance at this point of tipping it into economic viability.

The only reason the civilian leadership was able to muddle along this long is due to 0 percent fed funds rates from 2008-2009 until recently.

This allowed the totally economically unviable setup to fester instead of collapse for quite a long time.

This article that was already linked in another thread is a relatively polyanna-ish similar view on the situation.

Why the country fails

It is apparent now that Project Imran Khan/PTI is being dismantled. Some commentators wonder whether the PTI was ever a political party. Others use the past tense for the PTI. Whether or not the PTI...

www.thenews.com.pk

www.thenews.com.pk

Last edited:

Tell us how much China buys in Pakistani productsNo, it's not worth the ties we have with China and the fact that China is contributing actively to a massive economic project that could be a game changer for Pak.

CPEC - game changer ?? I need to sell you some more snake oil

Rosy scenario is not realistic:Pakistan's problems aren't actually that hard to fix.

The civilian leadership simply doesn't have any incentive to fix them.

'Pakistan's Foreign Exchange Reserves Will Fall To Zero By December'

Pakistan's current financial trajectory suggests that its foreign exchange reserves may fall to a zero by the month of December, analysts say. Khurram Husain

www.thefridaytimes.com

www.thefridaytimes.com

Mirzali Khan

SENIOR MEMBER

- Joined

- Sep 25, 2020

- Messages

- 5,855

- Reaction score

- -3

- Country

- Location

.,.,.,

Is Pakistan poised for default in FY24?

Khurram Husain

June 14, 2023

WITH dangerously low foreign exchange reserves and a steep debt repayment schedule looming for fiscal year 2024 that begins in July, Pakistan is facing a stark prospect of potential default or even a larger balance of payments crisis in the 12 months ahead.

Data obtained unofficially from a senior source privy to the country’s debt repayment schedule shows Pakistan faces $8.7 billion outflows on public debt payments in FY24 (including principal and interest) that are not subject to rollover.

On top of this, there is another $5bn approximately on private debt outflows as per the IMF staff report released in September 2022, bringing the total to $13.7bn in debt-related payments. Repayments on account of publicly guaranteed debt are on top of this.

The monthly schedule of outflows as per this government data is shown in the attached graphic. Assuming zero current account deficit, all rollovers going smoothly, debt payments made on time and no external financing support, the data shows State Bank’s foreign exchange reserves going negative by December of this year.

A large payment of $1.6bn is due in July, including $1bn of a Chinese SAFE deposit that is maturing and has been rolled over smoothly in all years since it was drawn. Government accounting convention requires it be listed as an outflow until a rollover date has been agreed between both parties. Should it be rolled over successfully again this year, July will still see a sizable outflow of $600 million.

June is already seeing hectic activity around debt repayments. In an analyst briefing following Monday’s monetary policy decision, the State Bank governor said $3.6bn was maturing this month, of which $400m has already been paid and another $2.3bn is likely to be rolled over.

“We have concurrence from both sides on this,” he told the attendees, though it seems a date has not yet been agreed because the amount is still being counted as an outflow. That still leaves a $900m further debt service bill in June to be covered from the reserves that are below $4bn already.

Of the total outflows on public debt account scheduled for the next fiscal year, $4.7bn is in July to December. April 2024 sees a large bond maturity when outflows leap to $1.2bn, and June 2024 sees another $1.5bn maturity of several instruments, only some of which are eligible for rollover.

If the government succeeds in the next few days in getting a rollover on the $2.3bn loan from a consortium of Chinese banks that was announced on June 22 last year, the scheduled outflow for June 2024 will rise to $3.8bn since these maturities will then fall due next June.

According to the last IMF staff report, private debt repayments on external account for FY24 are $5bn. These funds are also, under normal circumstances, rolled over fairly easily provided the borrower has been servicing the loan on time. Whether or not they’ll represent a drain on the reserves in the forthcoming year depends on the ability of these borrowers to continue servicing their loans in foreign exchange.

The same report shows Pakistan’s total public debt repayments to be just under $20bn, with another $1.68bn to be repaid to the IMF, and $13bn given as rollover on short-term debt. These numbers suggest outflows on public debt payments should be $8.7bn, consistent with unofficial government figures obtained by Dawn.

But this figure differs greatly from other numbers compiled by sovereign debt advisory firms and private creditors who hold Pakistani bonds. One such data panel, drawn up by a European firm and seen by Dawn, shows public external debt servicing for FY24 to be slightly higher than $14bn.

These creditors and firms triangulate their numbers from various sources, including databases maintained by Bloomberg, the World Bank and the IMF. When Dawn asked one of them for an explanation as to why their estimate for Pakistan’s debt service obligations for FY24 differs so widely from the one provided by the government, they offered various theories but were unable to reconcile the difference mainly because they could not agree on the assumptions that went into deciding which debt obligations will be rolled over and which ones will not.

“We never used this figure,” one individual, who has worked on estimating Pakistan’s debt service obligations, said, referring to the $8.7bn number. The person did not wish to be identified due to the sensitivity of the matter. “Because we never managed to understand what they assume will be rolled over.”

According to these individuals from the private sector, the $13bn assumed to be rolled over in FY24 seems too large. “I understand that this would include $7bn of SAFE and Saudi deposit, maybe $1bn of Islamic Development Bank facility. But I am having a hard time understanding where the other $5bn of rollovers come from,” he continued.

Complicating matters further, budget documents show repayment of foreign and short-term credits as $15.3bn in FY24. Against this figure, they show total external inflows to be $24bn, including $4.5bn in commercial borrowing, $4bn in a new SAFE deposit from China, $6bn deposits from Saudi Arabia and the United Arab Emirates and a $1.5bn international bond. How many of these inflows will actually materialise is another large question mark.

Whichever figure one takes — $8.7bn or $14bn or $15.3 — one thing is clear: there is no clear financing plan to meet these obligations for next year.

The government is projecting a current account deficit of $6bn. Coupled with the debt service payments, each of these figures yields an external financing requirement of either $14.7bn or $20bn or $21.3bn.

The plan chalked out by the government sounds optimistic in the absence of an IMF programme. And Finance Minister Ishaq Dar could have complicated the government’s efforts to secure the critical rollovers looming in June and July this year with his premature talk of a possible “debt restructuring”.

Seen from any angle, FY24 is going to see serious headwinds for the external sector, with ramifications for the exchange rate, inflation, and possibly even the integrity of the energy supply chain should the forex shortages intensify.

The country started FY23 with SBP reserves of $9.7bn. It made debt service payments of $9.7bn from July to April, and secured debt-creating inflows of $7.3bn in the same period, yielding a net drain of $2.4bn on the reserves. Coupled with a current account deficit of $3.3bn, the reserves fell by $5.7bn in this period.

No major covenants have been broken with the country’s external creditors so far. But for the next fiscal year Pakistan is looking at a higher debt service bill, very slim chance of securing further external financing support, and far lower level of reserves than last year.

The possibility of landing up in a situation where the foreign exchange reserves can no longer support even the basic life support systems of the economy is now a clear and present danger. If financing support does not arrive fast, the situation would have lingered too close to the edge for too long for a country of 220 million people.

Situationer: Is Pakistan poised for default in FY24?

Data shows State Bank’s foreign exchange reserves going negative by December of this year.www.dawn.com

Hopefully

That was always going to happen.Rosy scenario is not realistic:

'Pakistan's Foreign Exchange Reserves Will Fall To Zero By December'

Pakistan's current financial trajectory suggests that its foreign exchange reserves may fall to a zero by the month of December, analysts say. Khurram Husain

The problems, however, are very obvious and simple to fix.

A few of them were laid out in the article I linked.

The reason why the IMF and most countries are not willing to give Pakistan more money is due to those fundamental issues that create a giant hole in the bucket not being fixed.

The moment they are fixed, the IMF and most countries will be willing to lend again.

The problem isn't a lack of international will to help Pakistan.

The problem is a fundamental lack of Pakistani will to help Pakistan.

Atam bumb le Lo!! Taza Atam bumb le Lo!

2 crore! 2 crore fi kilo le Lo!

Thandar Tayarra! JF-satara .. 5 crore ke Darjan le Lo!

2 crore! 2 crore fi kilo le Lo!

Thandar Tayarra! JF-satara .. 5 crore ke Darjan le Lo!

Yes - this will all be fixed by military rule since they are not Pakistani??That was always going to happen.

The problems, however, are very obvious and simple to fix.

A few of them were laid out in the article I linked.

The reason why the IMF and most countries are not willing to give Pakistan more money is due to those fundamental issues that create a giant hole in the bucket not being fixed.

The moment they are fixed, the IMF and most countries will be willing to lend again.

The problem isn't a lack of international will to help Pakistan.

The problem is a fundamental lack of Pakistani will to help Pakistan.

Military rule would have to care less about maintaining vote banks in the short term.Atam bumb le Lo!! Taza Atam bumb le Lo!

2 crore! 2 crore fi kilo le Lo!

Thandar Tayarra! JF-satara .. 5 crore ke Darjan le Lo!

Yes - this will all be fixed by military rule since they are not Pakistani??

If they succeed economically, they will still be able to rule.

Of course, if they fail hardcore, they will be overthrown in time.

I went back and read that article. The author is wearing rose tinted glasses. Her prescriptions are 'simple':That was always going to happen.

The problems, however, are very obvious and simple to fix.

A few of them were laid out in the article I linked.

The reason why the IMF and most countries are not willing to give Pakistan more money is due to those fundamental issues that create a giant hole in the bucket not being fixed.

The moment they are fixed, the IMF and most countries will be willing to lend again.

The problem isn't a lack of international will to help Pakistan.

The problem is a fundamental lack of Pakistani will to help Pakistan.

1. Taxation

2. Privatization

3. Improved Human Capital

Now, there is nothing bad about any of them, in fact they are all very good. But they are not going to solve the basic problem: Pakistan doesn't make enough of anything that the world wants to buy compared to what Pakistan wants to buy from the world. That would need huge and sustained investment in both physical and human infrastructure. If done well, it is a multiyear program, more like multi-decade. Who is willing to finance that transformation? If you take the examples of India and Bangladesh, they took nearly two decades to go from near default to financial health. And they didn't have many problems that afflict Pakistan. The author herself says it will take 10-20 years to get out of coma. The question is, who will provide the lifeline?

Dalit

ELITE MEMBER

- Joined

- Mar 16, 2012

- Messages

- 23,622

- Reaction score

- -12

- Country

- Location

Pakistan was only balancing relations between the US and China as long as US-Chinese relations were good. As soon as the US decided to go into confrontation mode with China Pakistan has started siding with the US.

The generals have clung to the UK/US since the British left. They have their families and money in the West. Their retirement plans are in the West. Their weapon systems are from the West. Even most trade is with the West.

Knowing full well for decades that the US is not a reliable supplier of defense equipment the generals have made little effort to move away. Bajwa even admitted that they only buy Chinese weapons if the US refuses.

So, they’ve got no choice but to side with the US if forced to choose between it and China. The US knows that, so they don’t even bother to compete for Pakistan’s friendship.

India is buying defense equipment from both the US and Russia. America is trying to bribe India with massive investment and a strategic partnership. They’re installing Indians in high positions. India is milking them for everything it can get and still working closely with Russia.

Meanwhile Pakistan gets nothing. No investment, no IMF loans. The Americans don’t even have to pay bribes to the generals. The generals steal all the money they want from Pakistan and transfer it to America. All America had to do is look the other way and issue some green cards.

A few visas for the generals is all it takes to buy Pakistan.

The Americans know the DNA of Pakistani generals. Sellouts of the highest order. Complicit approvals and free of charge boot polishing. The Pakistani generals are some of the most greedy beings you will ever find.

I went back and read that article. The author is wearing rose tinted glasses. Her prescriptions are 'simple':

1. Taxation

2. Privatization

3. Improved Human Capital

Now, there is nothing bad about any of them, in fact they are all very good. But they are not going to solve the basic problem: Pakistan doesn't make enough of anything that the world wants to buy compared to what Pakistan wants to buy from the world. That would need huge and sustained investment in both physical and human infrastructure. If done well, it is a multiyear program, more like multi-decade. Who is willing to finance that transformation? If you take the examples of India and Bangladesh, they took nearly two decades to go from near default to financial health. And they didn't have many problems that afflict Pakistan. The author herself says it will take 10-20 years to get out of coma. The question is, who will provide the lifeline?

The Pakistanis are stuck with imbecile and inept leaders. This goes way beyond financial woes in my opinion.

Similar threads

- Replies

- 1

- Views

- 648

- Replies

- 0

- Views

- 310

- Replies

- 0

- Views

- 1K

- Replies

- 0

- Views

- 512