Black_cats

ELITE MEMBER

- Joined

- Dec 31, 2010

- Messages

- 10,031

- Reaction score

- -5

Xinjiang-Alternative Cotton Sourcing: A Brief Look at India, Pakistan, Bangladesh, and China

April 9, 2021Posted by India BriefingReading Time:8 minutes

RELATED SERVICES

The Xinjiang Uyghur Autonomous Region (XUAR) produces about 20 percent of the world’s cotton – and the province is China’s largest textile and apparel exporter. Raw cotton from XUAR is also spun into yarns used in factories worldwide, which means many companies are dependent on source inputs from XUAR – whether they are aware of this or not. After all, it is estimated that roughly one in five cotton apparel sold worldwide contains cotton or yarn sourced from Xinjiang. Eliminating XUAR-linked imports and sourcing outright may thus lead to supply chain shocks, particularly as the world is fighting a pandemic.

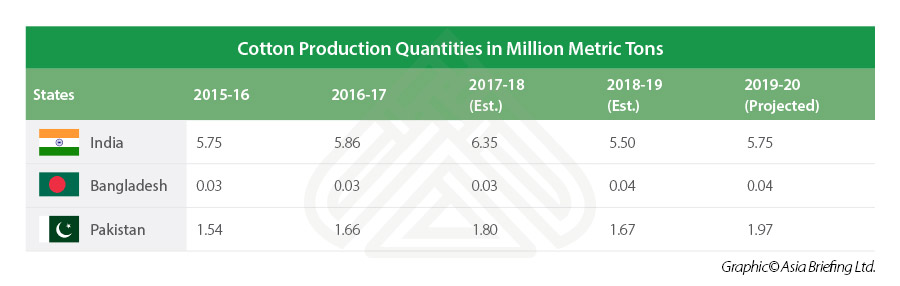

Below, we provide a snapshot of the global production of cotton and then briefly profile the regional cotton production status and general industry sourcing risk assessment for Bangladesh, India, and Pakistan. Lastly, we illustrate the lopsided growth of cotton production and related agro-industrial output across China.

Xinjiang-alternatives in the global supply chain for cotton: South Asia assessment

Bangladesh

According to the US Department of Agriculture’s Foreign Agriculture Service, Bangladesh’s raw cotton production was forecast to reach 146,000 bales in the marketing year 2020-21 and imports are expected to reach 7 million bales (showing a rebound in the sector demand since the pandemic struck last year). However, the Bangladesh Cotton Development Board (CDB) says that the country’s farmers have sown seeds on 44,450 hectares of land and expect production for the fiscal year 2020-21 to be 200,000 bales. This estimate is four percent higher than the production output in 2019-20, which was 177,890 bales. Bangladesh imported about 41 percent of its cotton needs from West Africa (Burkina Faso, Chad, Mali, Senegal) in 2018 and 2019, due to declining dependence on India because of quality concerns.

In terms of compliance risks for apparel companies, Bangladesh has made some progress in factory health and safety conditions. But its labor standards are a near constant thorn at the side for multinational firms sourcing from the country; the International Labor Organization (ILO) notes “the absence of a well-functioning labor inspection system” or decent enforcement mechanisms to ensure worker dignity and quality of life in Bangladesh. Since the collapse of Rana Plaza, which housed five garment factories, in April 2013, the ILO has reported about 109 accidents. Bangladesh also has a negative track record for recent actions against workers due to labor disputes and collective action, such as mass retrenchment and arrests (in 2019), as well as reports of unpaid garment workers during the pandemic.

Bangladesh features among the 10 worst countries for workers, according to the seventh edition of the International Trade Union Confederation (ITUC) Global Rights Index (that is, for 2020). The index ranks 144 countries on parameters related to worker’s rights.

India

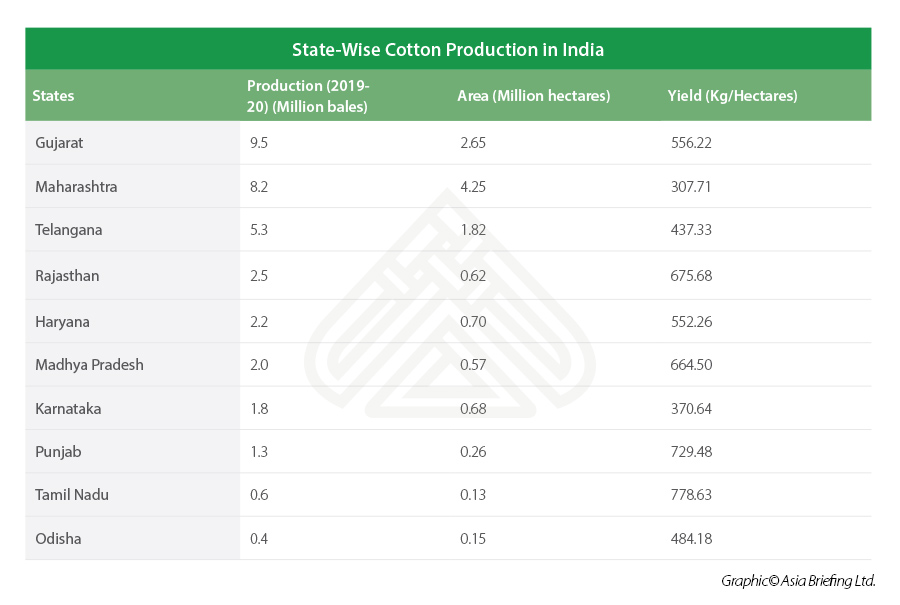

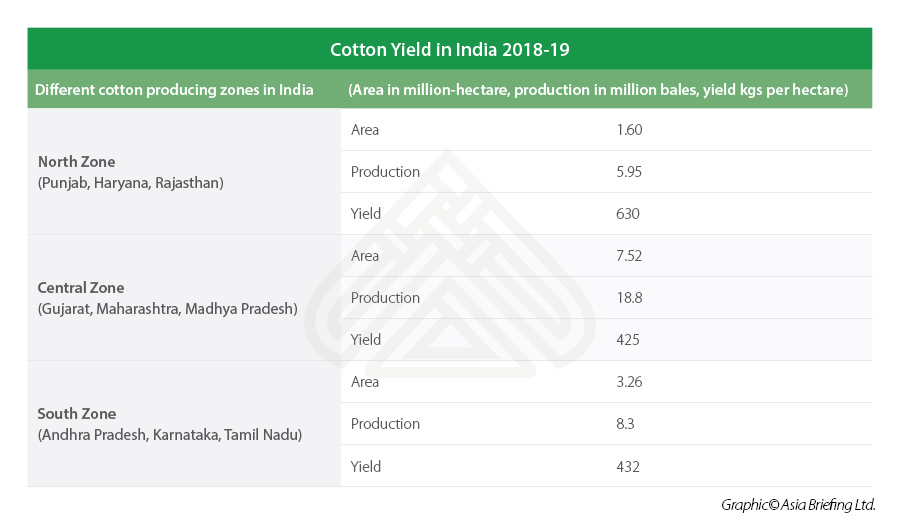

India has the largest area under cotton cultivation in the world – that is, 41 percent of the world area under cotton cultivation (between 12.5 million hectares to 13 million hectares). India is thus the largest cotton producer in the world, accounting for 26 percent of global cotton production. Yet, the average yields per hectare, at 487 kgs/ha, which is lower than the world average yield of about 768 kgs/ha. As per the Cotton Corporation of India, the crop area, cotton production, and yield for India in 2018-19, 2019-20, and 2020-21 are as follows:

A positive development, however, is that India’s cotton exports are projected to be 7 million bales in 2020-21, which is a growth of 40 percent and the highest in seven years. (The rupee’s depreciation and a rally in global prices allowed exporters to seal contracts.) On the other hand, as reported in the Financial Express, the South India Mills Association (SIMA) states that “India’s domestic consumption of cotton yarn is well below its production and its exports are also declining (from 1,313.43 million kg in 2013-14 to 959.79 million kg 2019-20 at a CAGR of about (-) 3%).” The combination of low domestic consumption and declining exports have led to surplus cotton yarn production in the country, in turn harming its spinning industry.

RELATED SERVICES

Despite being the world’s largest cotton producer and possessing a vertically integrated industry, India suffers from long-standing factors affecting quality output. The challenge for India is in consistently producing high quality yield, which is compromised due to its low yield rates, smallholder farms, and unorganized sector. In terms of exposure to compliance risks, multinational firms should note that labor rights in the country vary by geography, with reported practices of child and bonded labor in the agriculture sector. India features among the 10 worst countries for workers, according to the 2020 ITUC Global Rights Index.

Further, the country’s withdrawal from the Regional Comprehensive Economic Partnership (RCEP), a free trade agreement in the Asia-Pacific region, may present difficulties for improving its competitiveness with China in terms of exporting textiles to regional markets.

Additionally, India has struggled to attract significant amounts of foreign direct investment (FDI) in the sector due to lagging infrastructure.

India currently faces duty challenges in its export markets – Pakistan and Bangladesh levy higher duty rates on Indian yarn but they enjoy concessional or duty-free access to India’s market. India lags in access to global export markets due to duty disadvantage when compared to Bangladesh, Vietnam, and Pakistan. Also, while Bangladesh and Vietnam have duty-free access to China’s market, Indian exporters are levied duty.

India reportedly contributed 11.8 percent to the share of global exports of cotton, worth about US$6.3 billion, in 2019; China’s share was 26.6 percent of total worldwide exports at US$14.1 billion that year.

Pakistan

Pakistan’s annual cotton production fell by 34.35 percent to 5.571 million bales as of January 31, 2021 when compared to 8.487 million bales produced in the same period last year, according to the Pakistan Cotton Ginners Association (PCGA). Poor productivity has eroded export viability of the textile sector, which contributes 55 percent to 60 percent of Pakistan’s total exports. Cotton production in the province of Punjab was 3.436 million bales at the end of January this year as compared to 5.014 million bales produced in the same period last year, showing a decline of 31.5 percent.

Production in the Sindh province fared much worse, declining by 38.5 percent, and reporting 2.134 million bales produced at the end of January 2021 as compared to 3.472 million bales noted during the same time last year. In its FY21, Pakistan has had to import cotton worth US$321 million, reportedly raising costs for domestic textile manufacturers by 15 percent. Cotton production in the country has fallen for a third consecutive year, and the problem reported by growers is the quality of seed, which is 10 years old.

In terms of sourcing from Pakistan, the country’s reputation among international buyers is such that domestic producers have to work with intermediaries or route their supplies through nearby countries. In the case of the country’s garment exporting industries, factory infrastructure has reportedly improved, and foreign companies are usually based in designated economic zones that benefit from preferential policies targeting FDI. However, security threats remain a concern.

Sourcing from China: Lopsided regional cotton yield and production for exports

China leads the industrial value chain in most segments – cotton farming, yarn spinning, textile and fabric manufacturing, and garment cut-and-sew. Besides serving domestic manufacturing needs, China also exports yarn, fabric, and apparel to Bangladesh, Vietnam, Cambodia, and Indonesia who are all key players in the global supply chain.

A look within China, however, reveals that XUAR dominates other provinces in its cotton yield and production for exports. The region is China’s largest growing base of cotton. In 2020, the total cotton output in Xinjiang reached more than five million tons, accounting for 87.3 percent of that in the entire China. Shihezi, a sub-prefecture-level city in Northern Xinjiang, 150 kilometers always from Urumqi, is one of the primary producing areas of Xinjiang cotton, and is a textile hub for the country.

The Xinjiang province benefits from a combination of factors – ideal climactic conditions, low-cost production, infrastructure scale and high-tech machinery use, as well as vertical integration linking high quality raw material, processing, and intermediate inputs industries.

Outlook for apparel companies: International support and coordinated investments are urgently needed

The need for supply chain diversification in the textile and apparel sector has never been more urgent, and stakeholders will be actively assessing what needs to be done to achieve this.

At the outset, the development of new sourcing hubs would require at least 10 years, to ensure sufficient infrastructure, compliance with international human rights and environmental protection standards, worker upskilling and automation capacity, as well as vertical integration in the region so that an industrial ecosystem is established to achieve cost efficiencies and smooth supply.

This will cumulatively need long-term and strategic investments, besides developmental support and international agreements on concessional tariffs and trade arrangements.

Meanwhile, China’s own costs of production is rising, due to higher labor costs and a shrinking workforce, which had already triggered operational outsourcing to lower cost destinations. Nevertheless, the international consensus on labor standards – now in combination with geopolitical triggers – may serve as greater impetus for regional shifts in sourcing and distribution value chains.

Meanwhile, Asian countries outside China have been steadily working to scale up their capacity for exports and production (cotton, yarn, textiles) to varying levels of success. The focus in South Asian countries is also moving towards developing industrial value capabilities and technical textile production, away from raw material sourcing.

South Asia also faces challenges of yield rate and quality due to structural and technical challenges like patterns of land ownership and seed quality, which were further exacerbated by the COVID-19 pandemic. Duty and tariff arrangements in the region also hinder sourcing competitiveness when compared with the Chinese market. Finally, labor compliance risks persist in this region as well, a matter that is gaining prominence and affecting the brand image of many big name apparel companies. However, legal and worker reforms have been gradually introduced, and the application of international pressure has a record of producing positive outcomes.

About Us

India Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia from offices across the world, including in Delhi and Mumbai. Readers may write to india@dezshira.com for more support on doing business in in India.

We also maintain offices or have alliance partners assisting foreign investors in Indonesia, Singapore, Vietnam, Philippines, Malaysia, Thailand, Italy, Germany, and the United States, in addition to practices in Bangladesh and Russia.

April 9, 2021Posted by India BriefingReading Time:8 minutes

- Multiple reports concerning human rights violations, such as use of forced labor, in the Xinjiang Uyghur Autonomous Region have led to condemnation from many Western countries and put several multinational companies in a quandary.

- Xinjiang dominates global supply chains for cotton and apparel sourcing, which poses an immediate challenge for companies that cannot afford to shift cost-competitive sourcing contracts or do not find adequate alternatives.

- In this article, we briefly look at sourcing destinations in South Asia, namely, India, Pakistan, and Bangladesh as well as other provinces in China – to assess alternatives to Xinjiang in the global supply chain.

RELATED SERVICES

The Xinjiang Uyghur Autonomous Region (XUAR) produces about 20 percent of the world’s cotton – and the province is China’s largest textile and apparel exporter. Raw cotton from XUAR is also spun into yarns used in factories worldwide, which means many companies are dependent on source inputs from XUAR – whether they are aware of this or not. After all, it is estimated that roughly one in five cotton apparel sold worldwide contains cotton or yarn sourced from Xinjiang. Eliminating XUAR-linked imports and sourcing outright may thus lead to supply chain shocks, particularly as the world is fighting a pandemic.

Below, we provide a snapshot of the global production of cotton and then briefly profile the regional cotton production status and general industry sourcing risk assessment for Bangladesh, India, and Pakistan. Lastly, we illustrate the lopsided growth of cotton production and related agro-industrial output across China.

Xinjiang-alternatives in the global supply chain for cotton: South Asia assessment

Bangladesh

According to the US Department of Agriculture’s Foreign Agriculture Service, Bangladesh’s raw cotton production was forecast to reach 146,000 bales in the marketing year 2020-21 and imports are expected to reach 7 million bales (showing a rebound in the sector demand since the pandemic struck last year). However, the Bangladesh Cotton Development Board (CDB) says that the country’s farmers have sown seeds on 44,450 hectares of land and expect production for the fiscal year 2020-21 to be 200,000 bales. This estimate is four percent higher than the production output in 2019-20, which was 177,890 bales. Bangladesh imported about 41 percent of its cotton needs from West Africa (Burkina Faso, Chad, Mali, Senegal) in 2018 and 2019, due to declining dependence on India because of quality concerns.

In terms of compliance risks for apparel companies, Bangladesh has made some progress in factory health and safety conditions. But its labor standards are a near constant thorn at the side for multinational firms sourcing from the country; the International Labor Organization (ILO) notes “the absence of a well-functioning labor inspection system” or decent enforcement mechanisms to ensure worker dignity and quality of life in Bangladesh. Since the collapse of Rana Plaza, which housed five garment factories, in April 2013, the ILO has reported about 109 accidents. Bangladesh also has a negative track record for recent actions against workers due to labor disputes and collective action, such as mass retrenchment and arrests (in 2019), as well as reports of unpaid garment workers during the pandemic.

Bangladesh features among the 10 worst countries for workers, according to the seventh edition of the International Trade Union Confederation (ITUC) Global Rights Index (that is, for 2020). The index ranks 144 countries on parameters related to worker’s rights.

India

India has the largest area under cotton cultivation in the world – that is, 41 percent of the world area under cotton cultivation (between 12.5 million hectares to 13 million hectares). India is thus the largest cotton producer in the world, accounting for 26 percent of global cotton production. Yet, the average yields per hectare, at 487 kgs/ha, which is lower than the world average yield of about 768 kgs/ha. As per the Cotton Corporation of India, the crop area, cotton production, and yield for India in 2018-19, 2019-20, and 2020-21 are as follows:

- 2018-19

- 2019-20 (provisional estimate)

- 2020-21 (provisional estimate)

A positive development, however, is that India’s cotton exports are projected to be 7 million bales in 2020-21, which is a growth of 40 percent and the highest in seven years. (The rupee’s depreciation and a rally in global prices allowed exporters to seal contracts.) On the other hand, as reported in the Financial Express, the South India Mills Association (SIMA) states that “India’s domestic consumption of cotton yarn is well below its production and its exports are also declining (from 1,313.43 million kg in 2013-14 to 959.79 million kg 2019-20 at a CAGR of about (-) 3%).” The combination of low domestic consumption and declining exports have led to surplus cotton yarn production in the country, in turn harming its spinning industry.

RELATED SERVICES

Despite being the world’s largest cotton producer and possessing a vertically integrated industry, India suffers from long-standing factors affecting quality output. The challenge for India is in consistently producing high quality yield, which is compromised due to its low yield rates, smallholder farms, and unorganized sector. In terms of exposure to compliance risks, multinational firms should note that labor rights in the country vary by geography, with reported practices of child and bonded labor in the agriculture sector. India features among the 10 worst countries for workers, according to the 2020 ITUC Global Rights Index.

Further, the country’s withdrawal from the Regional Comprehensive Economic Partnership (RCEP), a free trade agreement in the Asia-Pacific region, may present difficulties for improving its competitiveness with China in terms of exporting textiles to regional markets.

Additionally, India has struggled to attract significant amounts of foreign direct investment (FDI) in the sector due to lagging infrastructure.

India currently faces duty challenges in its export markets – Pakistan and Bangladesh levy higher duty rates on Indian yarn but they enjoy concessional or duty-free access to India’s market. India lags in access to global export markets due to duty disadvantage when compared to Bangladesh, Vietnam, and Pakistan. Also, while Bangladesh and Vietnam have duty-free access to China’s market, Indian exporters are levied duty.

India reportedly contributed 11.8 percent to the share of global exports of cotton, worth about US$6.3 billion, in 2019; China’s share was 26.6 percent of total worldwide exports at US$14.1 billion that year.

Pakistan

Pakistan’s annual cotton production fell by 34.35 percent to 5.571 million bales as of January 31, 2021 when compared to 8.487 million bales produced in the same period last year, according to the Pakistan Cotton Ginners Association (PCGA). Poor productivity has eroded export viability of the textile sector, which contributes 55 percent to 60 percent of Pakistan’s total exports. Cotton production in the province of Punjab was 3.436 million bales at the end of January this year as compared to 5.014 million bales produced in the same period last year, showing a decline of 31.5 percent.

Production in the Sindh province fared much worse, declining by 38.5 percent, and reporting 2.134 million bales produced at the end of January 2021 as compared to 3.472 million bales noted during the same time last year. In its FY21, Pakistan has had to import cotton worth US$321 million, reportedly raising costs for domestic textile manufacturers by 15 percent. Cotton production in the country has fallen for a third consecutive year, and the problem reported by growers is the quality of seed, which is 10 years old.

In terms of sourcing from Pakistan, the country’s reputation among international buyers is such that domestic producers have to work with intermediaries or route their supplies through nearby countries. In the case of the country’s garment exporting industries, factory infrastructure has reportedly improved, and foreign companies are usually based in designated economic zones that benefit from preferential policies targeting FDI. However, security threats remain a concern.

Sourcing from China: Lopsided regional cotton yield and production for exports

China leads the industrial value chain in most segments – cotton farming, yarn spinning, textile and fabric manufacturing, and garment cut-and-sew. Besides serving domestic manufacturing needs, China also exports yarn, fabric, and apparel to Bangladesh, Vietnam, Cambodia, and Indonesia who are all key players in the global supply chain.

A look within China, however, reveals that XUAR dominates other provinces in its cotton yield and production for exports. The region is China’s largest growing base of cotton. In 2020, the total cotton output in Xinjiang reached more than five million tons, accounting for 87.3 percent of that in the entire China. Shihezi, a sub-prefecture-level city in Northern Xinjiang, 150 kilometers always from Urumqi, is one of the primary producing areas of Xinjiang cotton, and is a textile hub for the country.

The Xinjiang province benefits from a combination of factors – ideal climactic conditions, low-cost production, infrastructure scale and high-tech machinery use, as well as vertical integration linking high quality raw material, processing, and intermediate inputs industries.

Outlook for apparel companies: International support and coordinated investments are urgently needed

The need for supply chain diversification in the textile and apparel sector has never been more urgent, and stakeholders will be actively assessing what needs to be done to achieve this.

At the outset, the development of new sourcing hubs would require at least 10 years, to ensure sufficient infrastructure, compliance with international human rights and environmental protection standards, worker upskilling and automation capacity, as well as vertical integration in the region so that an industrial ecosystem is established to achieve cost efficiencies and smooth supply.

This will cumulatively need long-term and strategic investments, besides developmental support and international agreements on concessional tariffs and trade arrangements.

Meanwhile, China’s own costs of production is rising, due to higher labor costs and a shrinking workforce, which had already triggered operational outsourcing to lower cost destinations. Nevertheless, the international consensus on labor standards – now in combination with geopolitical triggers – may serve as greater impetus for regional shifts in sourcing and distribution value chains.

Meanwhile, Asian countries outside China have been steadily working to scale up their capacity for exports and production (cotton, yarn, textiles) to varying levels of success. The focus in South Asian countries is also moving towards developing industrial value capabilities and technical textile production, away from raw material sourcing.

South Asia also faces challenges of yield rate and quality due to structural and technical challenges like patterns of land ownership and seed quality, which were further exacerbated by the COVID-19 pandemic. Duty and tariff arrangements in the region also hinder sourcing competitiveness when compared with the Chinese market. Finally, labor compliance risks persist in this region as well, a matter that is gaining prominence and affecting the brand image of many big name apparel companies. However, legal and worker reforms have been gradually introduced, and the application of international pressure has a record of producing positive outcomes.

About Us

India Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia from offices across the world, including in Delhi and Mumbai. Readers may write to india@dezshira.com for more support on doing business in in India.

We also maintain offices or have alliance partners assisting foreign investors in Indonesia, Singapore, Vietnam, Philippines, Malaysia, Thailand, Italy, Germany, and the United States, in addition to practices in Bangladesh and Russia.

Xinjiang-Alternative Cotton Sourcing: A Brief Look at India, Pakistan, Bangladesh, and China

We briefly look at Xinjiang-alternative sourcing destinations in South Asia, namely, India, Pakistan, and Bangladesh as well as other provinces in China.

www.india-briefing.com