Assuring Taiwan’s Innovation Future

EVAN A. FEIGENBAUM

Summary: Taiwan’s innovation advantage is in danger of eroding. It needs a revitalized and broadened strategy, more diverse investments in human capital and next-generation industries, and forward-looking partnerships with the United States.

Related Media and Tools

Sign up for weekly updates from the Carnegie Endowment for International Peace

If you enjoyed reading this, subscribe for more!

Personal InformationE-mail *E-mail

EXECUTIVE SUMMARY

Innovation has been a source of comparative advantage for Taiwan historically. It has also been an important basis for U.S. firms, investors, and government to support Taiwan’s development while expanding mutually beneficial linkages. Yet, both Taiwan’s innovation advantage and the prospect of jointly developed, technologically disruptive collaborations face challenges.

For one, Taiwan’s technology ecosystem has been hollowed out in recent decades as personal computing (PC), component systems, and mobile device manufacturing moved across the Taiwan Strait to mainland China. Meanwhile, Taiwan’s innovation ecosystem has struggled to foster subsequent generations of startups to replace these losses in electronics manufacturing. Despite a freewheeling startup culture, internationalization has been a persistent challenge for Taiwan-based firms. Technological change and political challenges from Beijing present additional risks to Taiwan’s innovation future.

In this context, it is essential that Taiwan get back to basics if it is to assure its innovation advantage. One piece of this will involve taking a hard look at the domestic policy environment in Taiwan to ensure a steady pipeline of next-generation engineering talent. Yet Taiwan also needs to address several structural and policy factors that, over the last decade, have eroded its enviable innovation advantage.

Evan A. Feigenbaum

Evan A. Feigenbaum is vice president for studies at the Carnegie Endowment for International Peace, where he oversees research in Washington, Beijing and New Delhi on a dynamic region encompassing both East Asia and South Asia.

This paper examines five pressing challenges to Taiwan’s innovation future and proposes an array of specific solutions to promote Taiwan-based innovation, better leverage partnerships with U.S. and other international players, and bolster Taiwan’s standing in the global marketplace.

A particular focus is the need to foster a next generation talent pool with expertise in computer and data sciences, machine learning, and other fields that could contribute to the integration of software with Taiwan’s long-standing comparative advantages in hardware.

Taiwan’s innovation ecosystem has faced particular pressures on its ability to reorient from semiconductor and chipset design and fabrication toward new, future-facing industries. Many of the new systems in these industries do require advanced hardware. But they also require parallel adaptations in software, and the firms and national innovation systems that lead these industries tend to derive their competitive advantages from hardware-software integration.

To this end, forward-looking partnerships between Taiwan and U.S. players could naturally complement a revitalized and broadened innovation strategy for Taiwan.

INTRODUCTION

Innovation has been a source of comparative advantage for Taiwan historically. It has also been an important basis for U.S. firms, investors, and government to support Taiwan’s development while expanding mutually beneficial linkages.

But both of these things—Taiwan’s innovation advantage and the prospect of jointly developed, technologically disruptive collaborations—face challenges.

In the 1980s and 1990s, mutually beneficial collaborations between Silicon Valley and the broader Hsinchu-Taipei region supported entrepreneurial dynamics and the growth of the indigenous semiconductor and PC industries in Taiwan. In the 2000s, however, Taiwan’s technology ecosystem hollowed out as PC, component systems, and mobile device manufacturing moved across the Taiwan Strait to mainland China. Today, the Ministry of Economic Affairs (MOEA) annual survey has shown that over 80 percent of Taiwan’s information and communication technology (ICT)–related products are manufactured in China.1

Bluntly put, Taiwan’s innovation ecosystem has struggled to foster subsequent generations of startups to replace these losses in electronics manufacturing—for instance, in software, computer security, data, chips, and artificial intelligence.

But that is not all. Despite a freewheeling startup culture, internationalization has been a persistent challenge for Taiwan-based firms. A 2018 report from the Chung-Hua Institution for Economic Research concluded that while Taiwan’s total research and development (R&D) investment accounted for 3.05 percent of gross domestic product (GDP) in 2015, just 0.06 percent of private sector R&D activities are funded by foreign sources.2 Similarly, a 2018 PWC survey of Taiwan’s startup ecosystem revealed a significant lack of internationalization, with 71 percent of revenue sources for Taiwan-based startups generated by the comparatively small domestic market.3 Successful Taiwan startups with ambitions to expand overseas were revealed in this survey to lack the resources to do so.

This is just one of many areas that revitalized and strengthened partnerships between Taiwan and U.S. players could help to address. Taiwan-based startups appear keen to attract external investment, not just to obtain capital but also to plug into global networks.

Meanwhile, technological change and political challenges from Beijing present additional risks to Taiwan’s innovation future.

For one, Chinese state policies have thus far precluded Taiwan from forging industrial and commercial links in the context of formal investment, trade, or other framework agreements with regional governments, especially in the Southeast Asian countries that are critical parts of the East Asian manufacturing supply chain.

For another, the bleeding of talent across the Taiwan Strait has been a persistent challenge to Taiwan-based industry. Since 2017, Beijing has sought to ramp up its own domestic semiconductor industry, in part by poaching Taiwan-based talent.4 One recent report suggests that as many as 3,000 semiconductor engineers have departed Taiwan for positions at Chinese companies, a figure that would amount to nearly one-tenth of Taiwan's roughly 40,000 engineers involved in semiconductor R&D.5

In this context, it is essential that Taiwan get back to basics if it is to assure its innovation advantage.

One piece of this will involve taking a hard look at the domestic policy environment in Taiwan to ensure a steady pipeline of next-generation engineering talent. Yet Taiwan also needs to address several structural and policy factors that, over the last decade, have eroded its enviable innovation advantage.

Among the most important of these is the continuing concentration of Taiwan’s innovation strengths around hardware, even as the emerging and foundational industries of the future are increasingly being defined by hardware-software integration. There is no question that hardware will remain relevant to comparative advantage—for instance, through chips optimized to specifically perform artificial intelligence (AI) and especially AI on the edge-related functions. But the next era of chip design is in play, and partnerships and supporting policies to quickly research, develop, and test this hardware will be critical.

If Taiwan can secure its design data—and the data of its partners—while also securing its intellectual property from poaching and theft, it could reemerge as a key partner in multinational strategies to successfully shape the future market. Meanwhile, in various areas of AI (as well as an array of AI-enabled technologies, such as drones), success at integrating software with this new hardware will be the major point of differentiation in a truly global competition for advantage.

Another critical means to reinvigorate and assure Taiwan’s innovation advantage will be to focus on market-based rather than technology-based strategies. Yet because Taiwan itself, with just 23 million people, does not provide a market of sufficient size to support some such innovations, looking beyond the domestic setting by relying on third markets while broadening international partnerships will be essential to achieving scale.

The most successful market strategies are likely to be those that secure the emerging autonomy market. This includes AI-enabled markets in areas from bioinformatics to healthcare, the Internet of Things (IoT) to critical infrastructure protection, and, in time, quantum sensing and communications.

Speed, data crunching, and security at the edge will be major differentiators for those who become leaders in these areas.

There will be a strong technology strategy element to determining success. But tailoring those strategies to the emergent markets in these new industries will be the crucial long-term play. The tools that will enable manufacturing—and the manufacturing itself—including silicon- or bio-substrate, will be crucial to ensure strong and sustained growth in the mid to long term.

The good news is that there have been positive steps in Taiwan in recent years to redress at least some of these challenges.

For its part, Taiwan’s government initiated an “Asian Silicon Valley” project in 2016, with a base in Taoyuan and an initial budgetary outlay from President Tsai Ing-wen’s administration of 11.3 billion New Taiwan dollars ($350 million).6

Among other efforts under this initiative, the government subsidizes selected Taiwanese startup teams to spend a few months in Silicon Valley, normally with Valley-based accelerators. With the help of mentors from the accelerators, these teams have the potential to gain firsthand knowledge of the American market. That in turn can shape modifications to their products, services, and business models. They also come into direct contact with consumers and buyers beyond Taiwan itself. In select cases, they have found U.S.-based business partners and investors for their companies.

Similarly, the government adopted an action plan for enhancing Taiwan’s startup ecosystem in February 2018.7 This plan includes government backing for startups to participate in international accelerators and trade shows, as well as incentives for government procurement from startups and legal changes to the regulations governing the recruitment of foreign talent.

Beyond these government-sponsored efforts, however, private accelerators and “ecosystem builders” have also emerged.

One example is the Taipei-based Startup Stadium, which offers boot camps and other mentoring services aimed at helping local startups tap global knowledge and best practices, while also helping them try to scale for international markets.8 One illustration is in the area of fintech, where the Startup Stadium has connected the very modest number of Taiwan-based fintech startups to regional and global fintech accelerator programs.9

Other private Taiwan-based accelerators, such as AppWorks, have focused on new-generation fields like blockchain. And they have attracted not just local startups to their fold but also Southeast Asian startups that seek investment from Taiwan’s thriving venture capital industry and corporate partnerships in Taiwan.10

These successes demonstrate that international partnerships, particularly with U.S. players, could naturally complement a revitalized and broadened innovation strategy for Taiwan. The purpose of this paper, then, is threefold:

AnnaLee Saxenian of the University of California, Berkeley, has traced the basic contours of how IT-related industries became so central to Taiwan’s post-1980s growth story: In 1980, Taiwan’s IT output was less than $100 million.11 By 1989, it had grown to over $5 billion, and then grew by over 20 percent annually in the 1990s—a period when Taiwan’s GDP growth was in the 6–7 percent range—to about $21 billion in 1999.

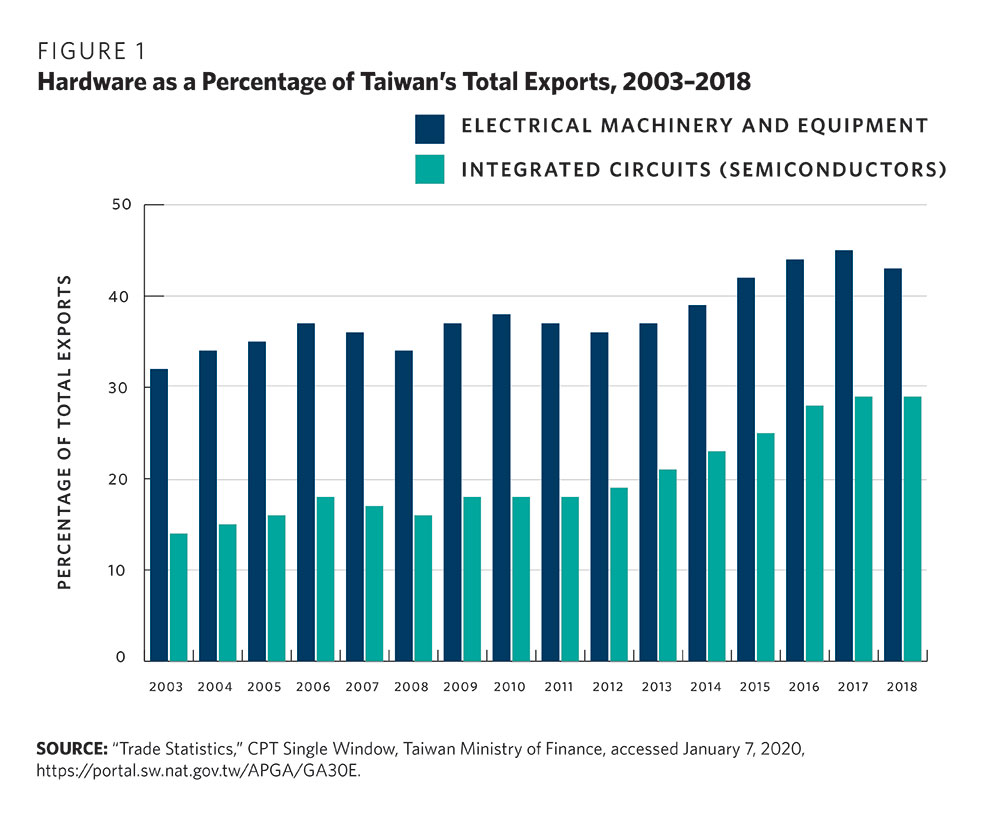

Ministry of Finance (MOF) data shows that advanced technology-related devices comprised a staggering 46 percent of Taiwan’s total exports for the first ten months of 2017, with the focus disproportionately on hardware as part of the global electronics supply chain.12

Not surprisingly, a single industry—semiconductors—dominates this picture, just as it has for nearly four decades. MOEA figures show that semiconductors accounted for 29.1 percent of Taiwan’s total exports in 2017 and, according to MOF data, a whopping 62.6 percent of its exports of technology devices.13 Three other hardware-related sectors—flat panels, wireless transmission devices, and mobile phones—comprised another 10.5 percent of the 2017 technology product export mix.

In fact, Taiwan’s dependence on hardware has only become more acute over the last decade. The same MOF data noted, for example, that these items have grown steadily as a proportion of Taiwan’s overall exports—from 39.5 percent of the total export mix in 2012 to 40.8 percent in 2013, 41.9 percent in 2014, 43.5 percent in 2015, 45.6 percent in 2016, and 46 percent in 2017 (see figure 1).14

The dominance of hardware, especially of semiconductors, reflects the core features of the three-legged model that made Taiwan so successful in the formative developmental period of the 1980s and 1990s.

The first leg of this model was the government’s competition policy, which played a crucial role in laying the foundations for Taiwan’s more flexible and decentralized model of hardware production at a time when bigger Asian economies chose a more centralized, less diverse pathway.

Taiwan’s government did not necessarily refer to its unique approach as “industrial policy.” Yet savvy technocrats, such as Li Kwoh-ting, invested aggressively in higher education. They promoted technology transfer, especially from the United States. They targeted R&D funds into electronics through the Industrial Technology Research Institute (ITRI), founded in 1973, and they launched an indigenous venture capital industry in Taiwan.

By contrast, Japan and South Korea established an especially close nexus between government industrial policy and a handful of large firms, such as the leading Korean chaebol. Taiwan’s model relied more heavily on strong market competition, which in turn supported a decentralized ecosystem and the development of technology startups.

Saxenian captured this dynamic well:

The dynamism of Taiwan’s IT industries, like those of Silicon Valley and its other “imitators,” [was] rooted in the incremental deepening and broadening of the capabilities of a localized cluster of specialist producers as well as in its close economic ties to the original Silicon Valley. This differs fundamentally from the privileged relationship between the state and a handful of large, established corporate giants that characterized IT development in Japan and Korea in the 1980s. If the East Asian case is viewed as state-led development, then the experience of Silicon Valley, Taiwan, and its other “imitators” is best understood as entrepreneurship-led growth.15

This points to the second leg of the model that undergirded Taiwan’s past success—internationalization, especially through links to the world’s leading global innovation ecosystem in California’s Silicon Valley.

Taiwan, in effect, discovered Silicon Valley decades before the rest of the world. That discovery—and the process of “brain circulation” of Taiwan-born but U.S.-educated and -trained engineers and entrepreneurs—in turn drove a wave of entrepreneurial growth in semiconductors, PCs, and other hardware-related industries.16

Taiwanese from the United States advised policymakers in Taipei during the 1960s and 1970s on economic development strategies, successfully advocating a focus on developing capabilities in leading edge technologies, such as semiconductors, rather than following the Korean model of moving into automobile manufacturing. They also worked with their peers at home. Some ultimately returned to Taiwan to take up leadership positions that helped expand the island’s system of higher education; its research capabilities, including the formation of the Electronics Research Service Organization (ERSO) and ITRI; and the development of a domestic venture capital industry.17

For these Taiwan-origin entrepreneurs and engineers who subsequently returned to Taiwan after education and work stints in Silicon Valley, the connection with California specifically and the United States generally provided a crucial store of knowledge, technology know-how, and strategies for market development.

This era was characterized by intensive exchanges of both hardware systems and underlying expertise between, on the one hand, California firms and individuals and, on the other, those in Taipei-Hsinchu. Soon, a set of transpacific social and professional networks formed.

Starting in the 1980s, this generation of returnees to Taiwan began to set up their own firms. Many of these became the backbone of Taiwan’s early wave of semiconductor, PC, and electronic systems producers. The new Taiwan-based firms subsequently forged additional and follow-on connections to Silicon Valley firms, who then set up their own manufacturing bases in Taiwan.

In this way, cross-regional partnerships facilitated mutually beneficial upgrading. Through a range of collaborations, including original equipment manufacturing and design (OEM/ODM) partnerships with leading U.S. firms, the competitive advantage of Taiwan’s manufacturers shifted from that of low-cost imitators to global leaders in electronics production based on speed, quality, and competitive costs.

A third leg underpinned Taiwan’s successful model: its ability not just to combine quality with cost advantage but to innovate independently. This is a feature that others, including China, have sought to replicate in their technology-based development strategies during recent decades.

Taiwan’s cheap labor advantage allowed it to quickly enter the global semiconductor market, which had been established in the United States in the 1950s by firms such as Fairchild (founded in 1957), National Semiconductor (founded in 1959), and Intel (founded in 1968). But Taiwan-based firms then quickly upgraded their quality, specialization, and production capabilities.

Probably the best example of this is Taiwan Semiconductor Manufacturing Company (TSMC), founded in 1987 by a Taiwanese returnee from Texas Instruments, Morris Chang, as a spinoff from the Li Kwoh-ting–inspired ITRI.

TSMC and other Taiwan-based market leaders in semiconductors and chipsets—such as United Microelectronics (UMC), founded in 1980 as another spinoff from ITRI—pioneered the dedicated semiconductor foundry business model, providing advanced chip production capabilities as a service.

All semiconductor firms at the time were vertically integrated, with both chip design and manufacturing conducted in-house. The foundry model proved to be a significant innovation because it allowed for the flourishing of new generations of firms that focused only on chip design and avoided the huge costs and complexities of production facilities.

Taiwan soon became a center of chip design expertise, with fabless chip design firm Mediatek (founded in 1997) as an early success story. Today, TSMC remains the world’s leading semiconductor fab, with cutting-edge production technologies and close to half of the global foundry market.

What makes TSMC so unique is both its mastery of chip design and its huge scale advantages. Its size means that it can spread out fixed costs and maintain lower per unit costs while pumping its considerable financial resources into next-generation R&D.

This three-legged model—smart government competition policy, aggressive internationalization, and the incubation of an independent innovation capability—yielded a highly decentralized and competitive manufacturing ecosystem. This promoted Taiwan’s leadership in semiconductor design and production, contributing to a flourishing period for its ICT manufacturing during the 1980s and 1990s. From the earliest days, the focus within this emerging ecosystem was on production for export, particularly of intermediate goods. The keys to the success of these globally competitive, Taiwan-based hardware firms became offshoring and comprehensive integration into global value chains.

But Taiwan’s sheer dependence on the IT sector in the overall export picture has been a critical and persistent theme in its economic development. Because that dependence has continued to this day, it has created vulnerabilities, even though champion companies like TSMC have capitalized on sales and supply chain opportunities to become globally dominant industry players in such areas as semiconductors and chips.

CHALLENGES TO TAIWAN’S INNOVATION ADVANTAGE

By the 2000s, this terrifically successful model was being increasingly buffeted by significant changes to Taiwan’s twin relationships with China and the United States.

With China, while much R&D remained in Taiwan, particularly critical semiconductor-related design knowledge, many hardware manufacturing supply chains shifted across the Taiwan Strait, especially to the Pearl River delta in Guangdong Province and the greater Shanghai region, because of cost advantages. By the middle of this decade, especially with the transition of mobile phones from a premium product to a globally popular one, the hardware ecosystem around the southern Chinese city of Shenzhen, in particular, had developed distinctive and dynamic characteristics.18 Above all, Shenzhen boasts rapid and efficient logistics to enable hardware innovators to design, prototype, and then repeatedly tweak and retweak a hardware product on very short production cycles. Today, that unique Shenzhen ecosystem mixes manufacturing prowess—much of it acquired from U.S., European, Taiwanese, and other Asian firms that set up fabrication shops there—with a deep stock of engineers.

With the United States, meanwhile, Taiwan saw diminished connections to Silicon Valley in the 2000s for two reasons: first, with more opportunities at home, fewer students from Taiwan came to the United States to study; second, Silicon Valley firms like Apple increasingly partnered with lower cost Chinese, not Taiwan, firms for their manufacturing needs.

This whipsawed the transpacific integrative model that had been so essential to Taiwan’s hardware success. It meant fewer connections to U.S.-based innovation and less of the intensive “brain circulation” that had characterized Taiwan’s formative period.

Meanwhile, U.S. innovators, including Silicon Valley’s principal market makers, increasingly shifted their focus away from hardware toward software—a shift that yielded new pressures on Taiwan’s hardware-dominant technology and innovation industries.

Above all, the Taiwan ecosystem has faced special pressures on its ability to reorient from semiconductor and chipset design and fabrication toward new, future-facing industries. Many of the new systems in these industries do require advanced hardware. But they also require parallel adaptations in software, and the firms and national innovation systems that lead these industries tend to derive their competitive advantages from hardware-software integration.

Around the world, there are useful models of successful adaptation whose features Taiwan could assimilate. Other economies, such as Israel’s and Estonia’s, have capitalized on these trends by forging niche advantages in cybersecurity and other new software-related industries. Singapore likewise aspires to be a fintech data hub.19 This has important implications for Taiwan because it demonstrates that small economies can be globally competitive if they both prioritize integration and decisively pursue specialization.

Still, the net effect of these changes has been that Taiwan’s ecosystem has fallen a few steps behind the United States, Canada, and other global technology leaders. Bluntly put, a new generation of Taiwan-based technology startups has yet to emerge. Indeed, while Taiwan now has a vibrant and flourishing startup scene, few of these firms have agglomerated around new or fast-growing areas of science, technology, engineering, and mathematics (STEM).

An overarching challenge, then, is for Taiwan to compete based on innovation rather than just continually moving up the value chain in legacy industries. In fact, this is a challenge for all economies, including the United States’.

But achieving this will require the concentration of resources, careful choices, and more strategic investments in knowledge-based industries of the future—for instance, those touching cybersecurity, big data, and such areas of artificial intelligence as machine learning and natural language processing.

Five major issues pose the most acute challenges to Taiwan’s innovation future:

STEM TALENT AND HUMAN CAPITAL

The first challenge—one that is front and center for Taiwan’s industry leaders—is an insufficient replacement pool of talented and qualified next-generation specialists.

Taiwan needs not just improvements to general STEM education but innovators with specialized skills in math, statistics, computer science, and data science. These skills lie at the heart of such emerging fields as machine learning, AI, and cybersecurity.

Taiwan faces gaps and shortfalls across the board in these areas. And this is compounded by dynamics in startup sectors, with company founders in Taiwan today disproportionately untrained in engineering or technical subjects, much less in specialized and emerging STEM fields.

PWC’s 2018 Taiwan startup survey starkly illustrates this gap. Of Taiwan-based startups surveyed, 70 percent had been founded by first-time entrepreneurs but just one-third of these had educational backgrounds in engineering (13 percent), science (7 percent), or information technology (13 percent). Nearly 60 percent of all Taiwan startup founders have backgrounds in the liberal arts or business disciplines. Nearly twice as many startup founders have backgrounds in marketing (14 percent) as in all of the sciences combined.20

Ironically, the lack of technically trained entrepreneurs who have established or worked in future-focused startups is a function of Taiwan’s remarkable past success. Indeed, so successful was the hardware-based manufacturing model that just two companies, TSMC and MediaTek, employ nearly 66,000 engineers.21 As a result, well-paid technical specialists have scant incentives to abandon their pivotal roles in a crucial industry by dipping their toes into the riskier world of next-generation startups.

But Taiwan’s broader talent base is also at risk. For one thing, Taiwan’s workforce is set to shrink. In 2018, Taiwan’s birthrate plummeted to an eight-year low of just 181,601 births, according to Ministry of Interior statistics.22 Taiwan now has the world’s lowest birthrate, with the National Development Council projecting meaningful declines as soon as 2021 or 2022, with likely negative effects on productivity as well as on the available pool of younger, educated workers available to the technology industry.23

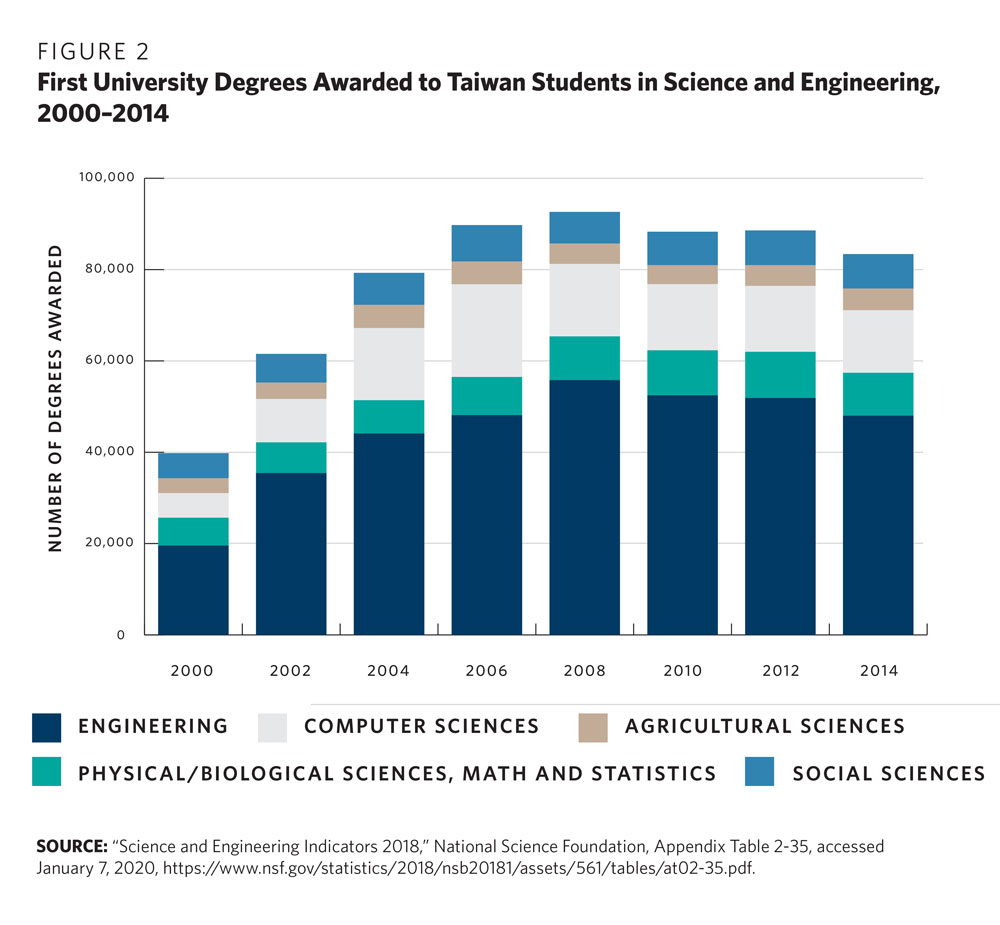

For another, Taiwan is producing fewer science and engineering graduates. From 2007 to 2014, the number of science and engineering first university degrees in Taiwan declined by nearly 10,000, from 92,167 to 83,394, although the total number of engineering graduates has risen sharply compared to, say, the 1990s.24 What is more, within this talent pool, the number of computer scientists and specialists in math, statistics, and the physical and biological sciences has not expanded in a significant way (see figure 2).

This means that Taiwan’s education system is producing insufficient technical talent while concentrating the talent pool that it does produce into legacy fields connected to semiconductor design, such as electrical engineering. Taiwan has underinvested in emerging areas, such as computer and data sciences.

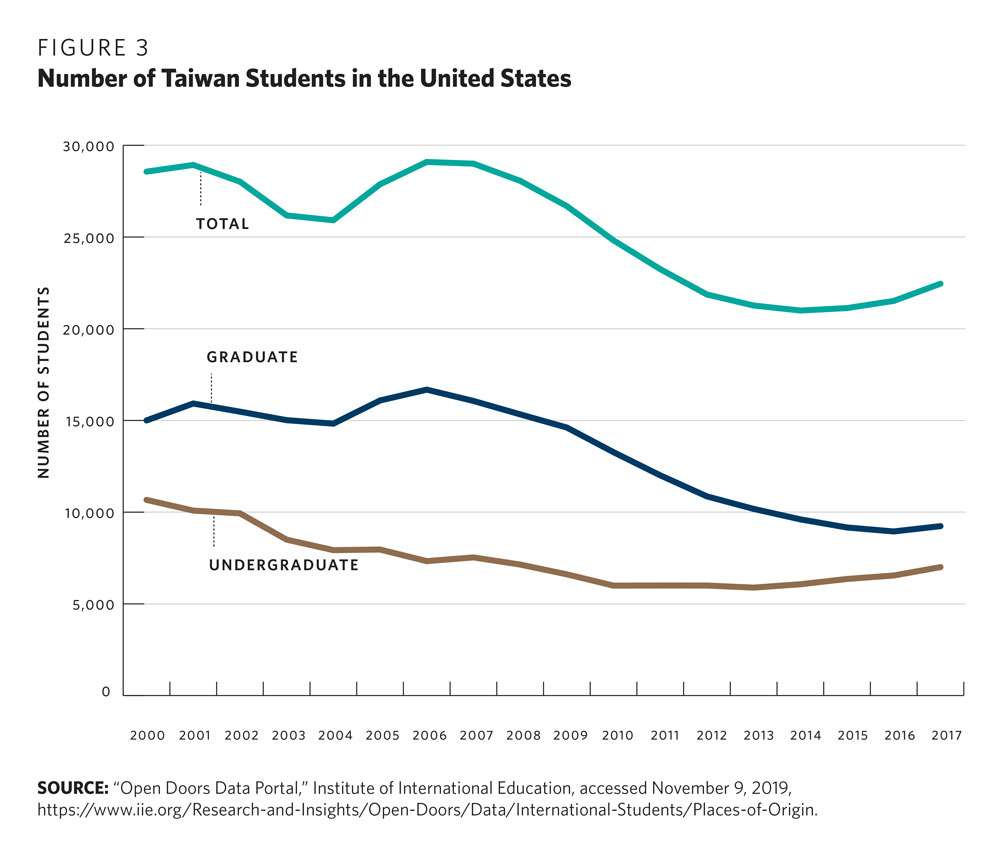

A related challenge is that the number of Taiwan students going to the United States for study has trended downward over the last twenty years at every educational level.25 Between 2000 and 2017, U.S.-bound undergraduates from Taiwan declined from 10,668 to 7,003, while U.S.-bound graduate students declined from 15,022 to 9,236 (see figure 3).

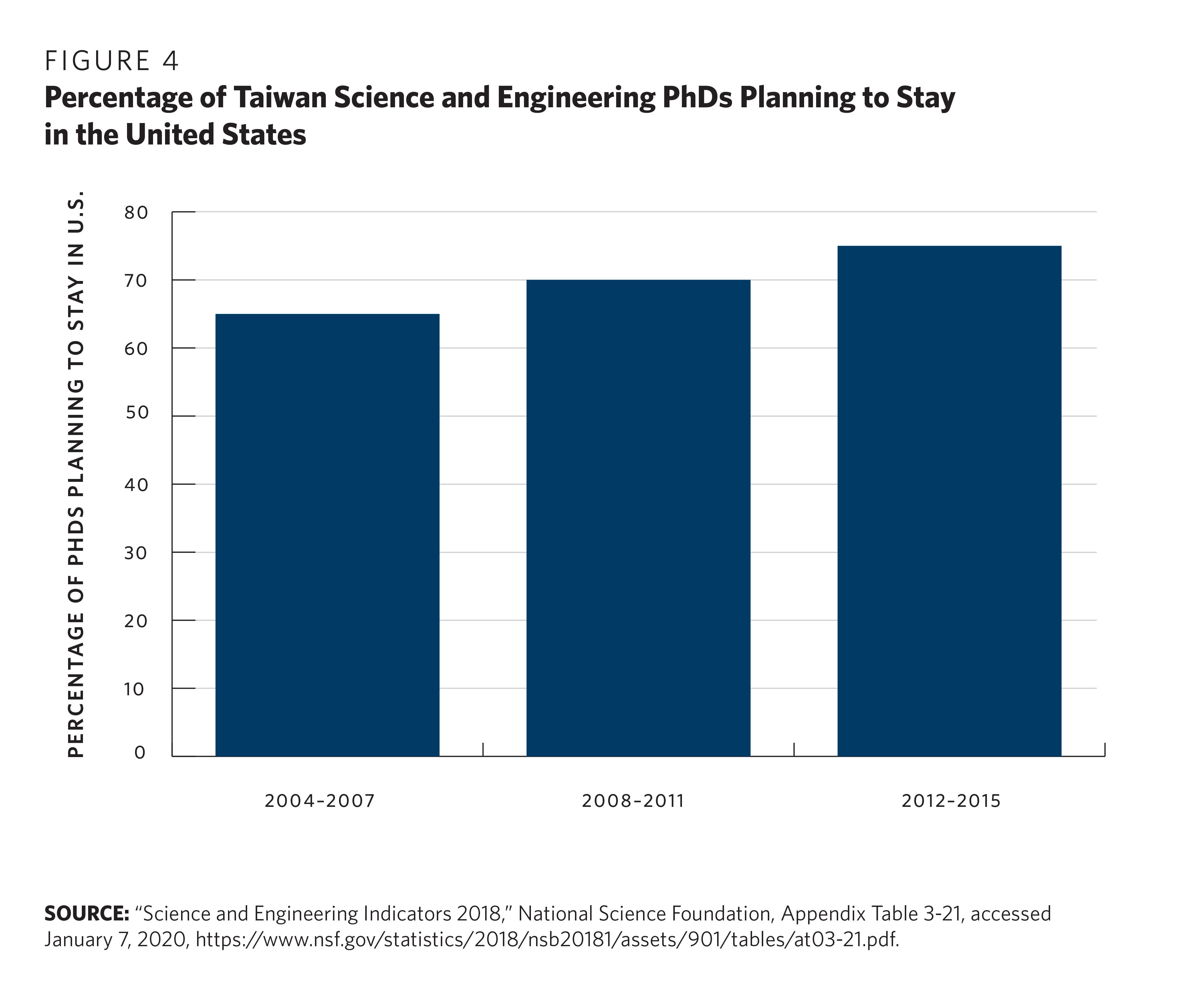

And more of these students, especially those with the most experience, are choosing to stay in the United States, not return to Taiwan. Roughly 65 percent of Taiwan-origin, U.S.-educated PhDs in the sciences and engineering planned to stay in the United States in surveys from 2004 to 2007—already a staggeringly high number. By 2012 to 2015, this number had risen to nearly 75 percent (see figure 4).26

This is important because so many of Taiwan’s initial successes of the 1980s and 1990s were enabled by “brain circulation” among Taiwanese returning home from the United States. Today, 3 of every 4 Taiwanese with American PhDs choose not to return home.

This will put a premium on forward-thinking educational initiatives, including public-private and international initiatives that aim to urgently ramp up Taiwan’s talent and skill base. Reinvigorated partnerships with universities and companies in the United States should, of course, be part of a next generation talent-building strategy.

Without more of these initiatives, Taiwan will face significant long-term headwinds. The AI industry today is being driven, in no small measure, by graduate and postgraduate students, much as computer science once was before the dot-com explosion. So, the fallout or mismatch between Taiwan’s STEM education and the need for talented experts who can drive the incubation of future-oriented industries in Taiwan will be acutely felt.

Any strategy must take into account the time needed to build and sustain expertise, as well as the flexibility needed to deploy it. A thoughtful STEM strategy for Taiwan focused not just on the engineering of hardware through electrical and mechanical engineering but also chemistry and biology as a substrate could help to produce both the disruptive force for the next market and the long-term foundation needed to sustain it.

Much of this challenge is, quite clearly, going to play out at the university level. But recent revolutions in technology have accelerated the pace of change. One Taiwan industry insider consulted for this paper argued that university curricula and new degree programs usually lag at least three to five years behind cutting-edge technology, and even this may be optimistic.27 So, Taiwan, like many other advanced economies, including the United States, needs to compete through enhanced STEM-related instruction at both high school and university levels. And where science and engineering education have tended to emphasize the hard sciences, new and emerging technologies—from AI to the Internet of Things (IoT) to blockchain—turn even more on specialized knowledge of software and data science, especially on mathematics and statistics.

Taiwan faces an additional challenge to its talent base: Beijing. Chinese markets have yielded high returns to capital, with a special segment of the mainland’s capital market devoted to technology, a good deal of flexibility built into it, and higher returns to investment in the Chinese technology segment than in Taiwan’s. That makes it an attractive destination for well-educated Taiwan technical specialists.

Beijing poses another problem too: brain drain from Taiwan to the mainland has been enabled by Chinese companies that have paid Taiwan-origin engineers as much as three to four times what Taiwan firms do. And Beijing has set into place both official and unofficial programs to attract and poach Taiwan’s talent.

The bottom line is this: Taiwan succeeded in the past through policies that attracted talented engineers back home from the United States. It would do well, then, to reinvigorate its ability to compete for global talent—from the United States, of course, but potentially from mainland Chinese expatriates too. The latter would be especially attracted by Taiwan’s comparatively better quality of life and the political openness of its democratic system.

SCALE

Taiwan’s small size also presents a barrier to creating scale in certain industries. Its population hovers around just 23 million, and the National Development Council predicts that Taiwan will likely bump up against a negative population growth rate by 2021 or 2022, with damaging effects on workforce composition.28

Scale and the resulting limitations of a small domestic market are not new problems for Taiwan. Other small markets have been able to foster large internet and platform companies—Spotify, for instance, was incubated in Sweden—but the underlying problem of scale is compounded by Taiwan’s urgent and growing labor skills challenge, which exacerbates handicaps associated with declining cost competitiveness. Scale problems could be better dealt with in the context of investments in a skilled labor pool and a STEM-enabled workforce.

Taiwan today largely cannot offer the unique manufacturing ecosystem of Shenzhen. That southern Chinese city does today what Taiwan did in the 1990s: speedy turnaround of low-cost manufactured electronic products. This is no longer an option for Taiwan because of its cost structure, where leading Taiwanese contract manufacturers, including Foxconn and Pegatron, which depend on low labor costs and huge supplies of unskilled labor, are doing most of their production in China. In Guangdong, labor and land have been abundant and they can leverage these operations to serve global markets. Taiwan, by contrast, can no longer itself house such cheap land and labor.

The good news is that capital is abundant and Taiwan’s venture capital (VC) industry remains especially strong. But one local industry player argued to this author that there have not been enough startup cases for Taiwan-based VCs to invest in for at least a decade. These essential VC funds have often been lost to mainland China, where they are being plowed into investments in China-based technology startups instead of into analogous firms in Taiwan itself.

A central challenge, therefore, will be how to attract not just Taiwan but also U.S. and international VCs and investors. This challenge is situated against the backdrop of a bubbly and potentially overvalued market in which Taiwan’s market capitalization has been comparatively high as a percentage of GDP, accounting for 159.8 percent of Taiwan’s nominal GDP in December 2018, down slightly from an all-time high of 177.0 percent a year earlier.29

The central dilemma in this basket of challenges is how to herd investments into next-generation industries and emerging fields. For AI, for example, Taiwan faces acute problems of scale for data. For quantum, it faces acute problems of scale for talent.

China and the United States have the clear edge in terms of sheer numbers of people. And China has worked hard to leverage a talent pipeline within that sizable population.

Just consider AI. One study notes that “Chinese-born researchers conduct a relatively small portion of the most elite AI research (~9 percent), but a substantial portion (~25 percent) of upper-tier AI research.” Another finding from the same study indicates that “while Chinese-born researchers have not quite scaled the peak of the AI research pyramid, they make up a sizable chunk of upper-tier AI research.”30

Notably, the bulk of these “upper tier” Chinese AI researchers (59 percent) work at U.S.-based institutions.31 This is important in two respects.

First, where the transpacific ecosystem that defined semiconductors and hardware innovation in the 1980s and 1990s linked Taiwan to Silicon Valley, the one that has now come to define AI links China to Silicon Valley. In effect, it is mainland China-based, not Taiwan-based, engineers and entrepreneurs who have forged the links to the United States that will define many aspects of the future of AI. Ironically enough, such a highly internationalized transpacific ecosystem between Beijing and California mirrors the internationalization and brain circulation that defined Taiwan’s past success.

Second, as technology-related competition accelerates between Washington and Beijing, many of these China-born AI experts may now leave the United States for home. This will likely further fuel the growth of AI research in major Chinese hubs like Beijing. In short, the “flow and retention” of Chinese AI talent may now reverse—from elite researchers building the U.S.-based industry to a returned cadre building AI firms in China.

This could have far-reaching effects on the competitive landscape for industries like AI.

But it could also buffet Taiwan, which has tried to achieve greater scale in part through closer economic links with the $14 trillion Chinese economy across the Taiwan Strait.

If trade and technology competition fracture the world into two camps, the private sector will try to straddle. Beijing is almost certain to ratchet up the pressure on Taiwan and its firms as they try to pursue economic integration elsewhere. Indeed, Beijing will continue to pressure Taiwan in multidimensional ways. And this is certain to be true of technology leadership, with Chinese firms continuing to try to poach Taiwan talent, among other effects.

Taiwan’s challenge will be to position itself as a more attractive alternative to China for multinational firms, globally oriented talent, and the R&D partnerships that define these nascent industries. There has been a spate of R&D labs of key global tech firms locating and/or expanding in Taiwan in recent years, including in emerging industries such as AI. These firms include global market leaders such as Google, Intel, Microsoft, and Qualcomm. This suggests the potential value of this play if Taiwan is able to leverage itself in these next-generation and emerging fields.32

BEYOND HARDWARE

Taiwan faces additional headwinds because of the concentration of so much of its comparative advantage into hardware manufacturing, just as next-generation industries are moving toward an emphasis on integration of software and hardware.

Drone technology is one example. Drones begin with high-quality hardware but have advanced rapidly on the basis not of progressive hardware tweaks but rather the application of advanced AI algorithms to the hardware. So, in this market segment, the ability to advance and adapt these AI technologies has defined the scope and outcomes of competition.

The global market leader in drones for aerial photography and videography is Shenzhen-based DJI, a Chinese firm that has captured 70 percent of the global market because of its advantage in flexible hardware manufacturing.33 Not surprisingly, it now seeks to make a transition to making AI and computer vision a new basis for growth. For DJI, that has yielded both global and U.S. partnerships, including one with Microsoft that uses edge computing to analyze data close to its source—namely, the sensors and computers that fly aboard the drone.34

But Taiwan will have a unique opening because of the growing aversion in some economies, not least the United States, to Chinese-origin AI technologies. Taiwan could potentially substitute for products designed or made in Shenzhen in such areas as intelligent robots and drones.

For example, suspicion of Shenzhen-origin technology could ultimately enhance Taiwan’s connections to the U.S. market. DJI’s partnership with Microsoft, after all, illustrates the strong interest in this area among major U.S. players, as well as the potential for new connections to the United States for the development of these technologies.

Yet a legacy ecosystem focused largely on hardware is unsuited to this opportunity. There will be a premium—and a substantial payoff—for technology-intensive economies best able to prioritize hardware-software integration.

Adaptive steps taken in other economies illustrate this: Taiwan could have, for example, innovated more rapidly to integrate its hardware advantage with software advances. Instead, other economies such as Israel and Estonia have taken a lead.

The good news is that Taiwan’s strengths in hardware are a necessary prerequisite to integrating new-generation software advances into future hardware advances. The bad news is that such integration can happen only if parallel efforts are now made to enhance and build complementary comparative advantages in software.

For instance, Taiwan could also have an opportunity to begin crafting the infrastructure of the bioeconomy through a focus on the biochip as infrastructure. Such technology, too, is about much more than just hardware. It integrates hardware, firmware, and software and could enable a huge new swath of the next-generation economy.

Engineering the flexibility into infrastructure to rapidly shift and grow as part of this next economy is a high-technology design problem with potentially huge payoffs. The infrastructure and tools necessary still need to be designed and developed, so the time for Taiwan to educate and build in this space is now.

VALUE ADDED FOR TAIWAN

The East Asian manufacturing supply chain, including in electronics, is also evolving rapidly. Movement out of China to Vietnam, Malaysia, and Indonesia, among other locales, began in the last decade because of rising Chinese labor costs. But now unilateral, reciprocal, and retaliatory tariffs flowing from the U.S.-China trade war since 2017 have accelerated this organic process, particularly for low- and mid-end products.35

This story is more complicated, however, for higher-end manufactured products—for instance the microelectronic components produced in Guangdong by Taiwan-headquartered Foxconn. South China’s well-established and smoothly functioning manufacturing ecosystem cannot be moved or replicated so easily.

Alternative locales, such as Thailand and Vietnam, are limited in their capacity to absorb these types of manufacturing. The establishment of new Foxconn facilities in India has mostly aimed not at the integration of India-based facilities with the broader East Asian manufacturing supply chain but at servicing India’s huge domestic smartphone market. Foxconn’s India-based facilities make most of their devices for companies like Xiaomi, whose competitively priced smartphones are especially popular in India.36

Taiwan’s challenge, then, is twofold.

First, it can grab a slice of the rapidly evolving manufacturing chain but focus on higher end manufacturing and especially the emerging AI and quantum value chains. These center primarily on big platform companies, such as Amazon and Google in the United States and Baidu, Alibaba, and Tencent in China, and on second-tier unicorn firms like China’s Bytedance and Pinduoduo.

Second, Taiwan can seek to innovate in areas where one does not find these big platform companies, which mainly serve consumer markets. There is considerable opportunity to integrate software, AI, and data science into established industries ranging from healthcare to education to information security.

The success of both platform and niche firms yields two lessons.

One, AI is a data-driven enterprise. Thus, big companies often have the edge because their sheer size means they naturally acquire huge troves of data.

Second, big data is not the whole story of the AI value chain. Some new algorithms require less data to train and thus could be useful market segments for Taiwan to target in upgrading its R&D capabilities.

Moving more of Taiwan’s economy into those segments will be a challenge because, for the last twenty years, Taiwan’s efforts to move beyond low-value-added manufacturing through upgraded R&D have yielded mixed results. Manufacturing today accounts for just under 30 percent of Taiwan’s GDP and job creation. Yet Taiwan ranks five to six points below leading countries in value added—with the exception of the ICT and semiconductor sectors.

Two Taiwan firms, both of them established market leaders in this segment—TSMC and MediaTek—are highly competitive in terms of value added. Yet the majority of large Taiwan manufacturers remain well behind these two firms.

The challenge Taiwan faces today is analogous to the one facing China’s Greater Bay Area (GBA), another leading electronics manufacturing center. Like Taiwan, government and industry leaders in the GBA aim to move into advanced technologies, including AI and data-driven fintech. But the most successful Shenzhen startups, like drone maker DJI, are already combining precision hardware manufacturing capabilities with an array of AI applications. These Chinese companies have an advantage over prospective Taiwan competitors because of the huge scale of the mainland’s domestic market and links to the global market.

Still, this need not be a zero-sum game. There will be considerable opportunities for innovation with new software and technologies. Taiwan’s best course is to complement global trends by developing new, high-end manufacturing and R&D capabilities that leave a larger share of value added in Taiwan itself.

This will compensate for the smaller scale of its domestic market when compared to, say, China or India. For example, new semiconductor and AI investments could aim to complement the U.S. buildout of cloud and quantum computing.

POLICY ENHANCEMENTS

The visionary behind Taiwan’s economic miracle Li Kwoh-ting and other pioneers of Taiwan’s growth story demonstrated that policy decisions and effective signaling to businesses and markets can incentivize entrepreneurship.

The current government has tried to draw lessons from their example with President Tsai Ing-wen’s launch of the so-called 5+2 Innovative Industries Plan.37 This plan aims to move seven industries and areas beyond their roots in contract manufacturing into high-value-added businesses and services:

Still, many aspects of these government plans remain declaratory and aspirational. The government has, for example, identified ways to boost investment in AI research but has not articulated a strategy to target particular niches for specialization.

The United States and Europe, by contrast, have developed such strategies. So has Japan for AI-related healthcare, with the government establishing ten AI-enabled hospitals to serve a Japanese AI healthcare market expected to reach US$100 million by 2025.39

Beijing is likewise pursuing AI-enabled facial recognition technologies in a highly strategic fashion, steering contracts and opportunities to global market leaders like Megvii—a Chinese unicorn that has recently been added to the U.S. Commerce Department’s Entity List.40

The lesson—once again—is that a comparative advantage in hardware is important, but this, by itself, will not set Taiwan up for the industrial and technological challenges of the future.

An entirely new set of policy signals will be needed for a new era. Specifically, Taiwan needs the ability to absorb timing mismatches driven by longer-than-anticipated technology development in some market and infrastructure areas. The government should seek to enable an environment conducive to foreign investment in these segments. That also means that well-intentioned government policies toward both foreign and domestic investors should not be burdened by cumbersome and costly tax schemes.

SOLUTIONS AND PARTNERSHIPS

As it seeks to recalibrate and enhance its longstanding innovation advantages, Taiwan should aim to overcome these five obstacles. More focused policies and strategic investments are needed. So too are enhanced international partnerships, particularly with the United States.

It was the Taiwan–Silicon Valley connection, after all, that contributed so much to Taiwan’s first-generation talent pool and the creation and subsequent dominance by Taiwan firms of essential hardware industries. A new generation of Taiwan-U.S. partnerships, built on a forward-looking foundation that works to overcome these five challenges, could play an analogous role today.

STEM TALENT AND HUMAN CAPITAL

Taiwan would be better positioned to play this role if it could enhance its status as a truly bilingual economy. Alongside bolstered investments in STEM education, English language facility will be an essential ingredient of Taiwan’s efforts to overcome the challenges of scale by internationalizing and playing a mediating or conduit role regionally and globally.

What is more, Taiwan could make itself into a regional hub for high-tech education by offering engineering programs in English, in particular for the electrical and mechanical engineering requisites of semiconductors and chipsets. Students from Southeast Asia, South Asia, and other parts of the world may find the cost of engineering programs in the United States, Europe, or Australia to be prohibitive. So, Taiwan should aim to make itself into the next alternative for international students in these specialized areas of engineering.

Yet the central question for Taiwan is whether it can cultivate a STEM talent pool not for right now but for ten to twenty years down the road—a pool that combines technical with operational and business skills, focuses not just on hardware but software and integration, and moves beyond traditional strengths in semiconductors and chips into fields like AI, quantum, and cybersecurity.

Taiwan could enable this through several steps in the area of university-industry partnerships:

For one, the government and industry should partner to establish university-based startup incubators, perhaps mirroring the areas under the 5+2 program with a cluster of incubators at certain universities—or else one incubator for each of the seven industries—spread among distinct locales.

A model of sorts already exists in Taiwan’s semiconductor industry. As public funding declines, industry players have agreed to furnish matching funds for university professors and laboratories. This government-industry match funding model could be extended to next-generation fields.

To hedge against the short-term return-on-investment (ROI) focus that dominates the venture capital community, this startup incubator effort should be tied to, and ultimately supportive of, the longer-term ROI of retooling and supporting next-generation infrastructure.

Second, Taiwan should look to marry technical with business training. The government could encourage business schools to integrate technical training into their curricula, endowing programs and financing courses of study in computer science and IT at these institutions.

The reverse is also true: institutional partnerships could be better leveraged to help business schools teach operational skills to those enrolled in Taiwan’s technical and engineering schools. Taiwan has strong hardware and improving software talent, after all, but a much weaker supply of international operational talent.

Such an effort to merge technical with internationally oriented operational talent is especially needed to build Taiwan’s startup sector.

The 2019 PWC Taiwan startup survey reveals that local startups are disproportionately anchored in Taiwan’s domestic market. This is as true of their talent base as it is of their market orientation and operational focus: 60 percent of Taiwan-based startups have not begun hiring or fostering international talent. As many as 54 percent have not approached foreign markets in expos or pitches, and just 30 percent have even begun to evaluate target foreign markets.

In short, even if Taiwan-based startups are able to leverage technical skills and disruptive technological breakthroughs and ideas, they would lack internationally oriented managers who could help to build the businesses by leveraging these technologies for markets outside Taiwan.

The most acute need of all is for aggressive steps to assure a steady pipeline of STEM talent as Taiwan builds knowledge-based industries.

Israel provides reference points for one potential model. The Israeli Talpiot program has trained top military recruits in technical subjects.41 Talpiot graduates have provided a stream of technology talent to the country’s vibrant startup sector, with some graduates founding companies including Check Point, Compugen, Anobit, and XIV (the latter two having been subsequently acquired by Apple and IBM).

Israel fostered an enviable startup-friendly nexus between government, industry, and universities. As one example, Israel made a commitment to move units of its intelligence service to the town of Be’er Sheva, and that unit’s members became eager to look for startup opportunities once they finished their three-year (or longer) commitment to military service. Then, they were able to apply the technical knowledge they gained in the military to private ventures, including an array of successful technology startups.

For its part, Israeli industry agreed to colocate R&D units in Be’er Sheva with VC firms, which also established a presence there. Taken together, this provided access to larger companies and financial fuel to support the growth of a startup ecosystem. Finally, Ben Gurion University was the academic partner for this effort, injecting research into business ideas and providing the space to test and “red team” innovations.

The Be’er Sheva model is just one example of how a strategic approach that marries government, industry, and universities can foster a tech- and startup-friendly ecosystem.42 Like Taiwan, Israel confronts a scale problem: with just 8 million people, its population is nearly two-thirds smaller than even Taiwan’s. And much like Taiwan, it also faces strategic pressures from larger neighbors and is vulnerable to those strategic pressures and disruptive global economic trends.

Some elements of Israel’s model may be adaptable, specifically:

But Taiwan’s government should take other forward-looking steps to build the pipeline too:

To overcome some of the challenges of its small-scale domestic market, Taiwan needs a three-pronged strategy: Taiwan must be a hub, a trusted vendor, and a conduit. Such a strategy could be leveraged to operate on a global scale even though its economy is comparatively smaller than its giant neighbors.

Taiwan as Hub

Above all, Taiwan should aim to become a hub for a new generation of knowledge-based industries, products, and services. But that will be no easy thing in a competitive marketplace where the technologies in question, particularly those that integrate AI applications, rely heavily on big data.

The bigger the market, the larger the available data sets. So, logically, more access to more data will give a firm anchored in a larger marketplace a comparative advantage. Yet as Matt Sheehan has argued, “data is not a single-dimensional input into AI.” While it is true that China, the United States, and India, for example, have large populations and more access to domestic data than Taiwan, “the relationship between data and AI prowess,” Sheehan argues, “is analogous to the relationship between labor and the economy.” For example, “China may have an abundance of workers, but the quality, structure, and mobility of that labor force is just as important to economic development.”44

Put bluntly, data quantity matters but so too does data processing, synthesis, and deployment. That is precisely why small economies, including Israel and Estonia, have been able to overcome their small scale by prioritizing sectors, capabilities, and specific parts of the knowledge industry value chain.

One solution, then, would be for Taiwan to emulate and adapt another Israeli example—becoming an industry- and service-specific hub in cybersecurity.

Specifically, Taiwan’s government could define a comparative advantage against larger economies by enabling access for its own startups to high-quality government data. In China, firms have been given increasing access by the government in Beijing but the data itself is of low quality. In the United States, firms tend to have low access although the data itself is actually of high quality. Taiwan could distinguish itself from both China and the United States if it can marry these two pillars by assuring both high quality and easy access for some nonsensitive public sector data sets.

In addition, Taiwan could further leverage an effort to make data a comparative advantage by building on its role as a leader in data protection and privacy standards. Taiwan has strong laws in place, especially when compared to those in mainland China and Southeast Asia. And these are an attractive selling point for Taiwan-based partnerships with U.S. and global firms.

Several specific steps could help in this regard:

What will drive the emergence of a next-generation economy is the development of tools to enable its creation. Becoming a center for the tooling of economies of the future could become an advantage for Taiwan and the United States in a new Taiwan–Silicon Valley partnership.

Taiwan as Trusted Vendor

Earning a reputation as a trusted vendor or supplier can be the second dimension of dealing with Taiwan’s scale challenge.

The government should look to enhance the 5+2 Innovative Industries program with a complementary trusted vendor certification program (TVCP), deploying the weight and credibility of the state to incentivize specific standards in specific emerging industries and then leveraging this advantage with foreign partners.

Amid growing U.S.-China tensions and increased suspicion of China-origin advanced technology products, demonstrating that Taiwan is a secure and trusted partner could help to compensate for the mainland’s obvious scale advantages. This environment could be conducive to fresh partnerships between Taiwan and U.S. universities as collaboration with mainland institutions falls out of favor.

It could also help to reinvigorate Taiwan’s once-intensive connection to Silicon Valley. Alongside a trusted vendor program, Taiwan should pursue a trusted tester effort—taking steps to make Taiwan a preferred location for knowledge-intensive U.S. technology products to be tested for cyber, 5G, and AI-related applications. One way to do this would be to develop sister cluster partnerships with U.S. innovations hubs, not just in Silicon Valley but in Japan and Europe too.

Taiwan as Conduit

Taiwan should also continue to advertise itself as a more trusted gateway than mainland China to Southeast Asia’s fast-growing markets for knowledge-intensive products and services. U.S. firms hope to market such knowledge-intensive products to Asia writ large but often lack some of Taiwan’s advantages. Especially for smaller and midcap U.S. firms, Taiwanese partners could serve as a conduit.

Taiwan can also be both conduit and trusted partner in the context of linkups between its New Southbound Policy and the U.S. Indo-Pacific strategy. One pillar under the U.S. effort is a “digital connectivity and cybersecurity partnership” program.45 South Korean companies, for example, are now actively working with the United States on cybersecurity capacity training for the Southeast Asian market.46

Taiwan’s rich network of corporate and industrial relationships, combined with its emphasis on the region in the New Southbound Policy, argue for a similar effort through which the United States and Taiwan seek complementary or joint opportunities to enhance Southeast Asian capacity in this and related areas.

BEYOND HARDWARE

With competition intensifying in software-enabled industries, Taiwan should prioritize carving out a specialized niche in the newly emerging, rapidly evolving global value chains for knowledge industries like AI and IoT.

The focus should be in two areas. First, Taiwan needs to catch up in global user-centric ecosystems and business models, and second, Taiwan needs to choose areas closely related to its current industrial base because two decades of brain drain have taken a toll on the size and diversity of the overall STEM workforce.

Taiwan’s success in the 1980s and 1990s was rooted in policies that encouraged a flexible and decentralized ecosystem. More recently, the global success that smaller economies have had with niche industries and applications demonstrates that concentration can also play a role.

With ecosystems for new industries still emerging, increased specialization and focus could be to Taiwan’s advantage in areas, such as data integration, that will be important in the rollout of 5G and IoT. Indeed, Taiwan has innate strengths here on the hardware side. For instance, MediaTek is soon to launch its 5G chip, which will be one of just four 5G chips globally alongside those from Huawei, Qualcomm, and Samsung.

Taiwan may also develop opportunities in quantum computing as a result of the 2019 opening of “IBM Q,” a co-innovation hub of IBM and National Taiwan University. To date, Taiwan has had fewer uses for quantum at scale. Such hubs give Taiwan an early opportunity to become “quantum ready” just as R&D on this next generation computing technology advances to its pivotal stage.47

VALUE ADDED FOR TAIWAN

With the East Asian manufacturing supply chain evolving rapidly, not least in electronics, U.S. firms are among those reconsidering whether high-end manufacturing is overconcentrated in some Asian locales. The U.S. government, in particular, is eager to discourage high technology dependence on China-based suppliers.

This should yield at least some new opportunities for Taiwan-based manufacturing because supply chains are almost certain to remain concentrated in Asia, with few firms able to establish such facilities in the United States itself. For instance, some manufacturing supply chains have begun to relocate from China to Taiwan, notably in the ICT industry, including those making servers and telecommunications products. These firms relocated not just to avoid the punitive tariffs imposed by Washington as part of the U.S.-China trade conflict but also to ensure cybersecurity. Because the integration of hardware with software is essential to these products, parallel investments by related U.S. software companies would further bolster industrial change in Taiwan.

Beyond ICT, Taiwan needs to secure new industries that would bring greater diversity to its industrial structure. One example could be electric vehicles (EVs) because this would provide new opportunities for Taiwan-based electronics firms to join the global supply chains of an emerging industry.

There are other potentially promising sectors too. The fact is, the United States cannot go this alone: it will need partners to drive next-generation infrastructure and tooling in hardware, AI/IoT trusted infrastructure, and even biotechnology.

That is why new U.S.-Taiwan university partnerships designed to support such a future could be incentivized in Taiwan as a hedge against Beijing’s long-term STEM efforts. The incubator model is important but not sufficient. For enduring STEM partnerships linking Taiwan and the United States, security should be baked in from the start of design in such areas as AI and IoT.

If Taiwan can succeed at setting high or even best-in-class security standards—for instance, through the efforts described above to become a trusted vendor, trusted tester, trusted conduit, and trusted research hub—it could enable enhanced knowledge partnerships with the United States.

POLICY ENHANCEMENTS

Finally, Taiwan’s government can take some additional policy steps.

The role of government in any national innovation system is often described as that of a facilitator, enabling the private sector to exploit the economy’s current comparative advantage while strategically guiding a shift toward new areas.48 That well describes Taiwan’s legacy of success. As noted in a recent IMF report, after all, nothing about Taiwan’s factor endowments predisposed it to a comparative advantage in semiconductors in the first place.49

Yet one important lesson of Taiwan’s experience with semiconductors is that, much as was the case with hardware, Taiwan’s next advantage will likely emerge only through targeted and sustained investment. Boosting research spending should be a particular priority: for long-term investment in emerging technologies, Taiwan’s government will need to administer a steady supply of “patient capital” to enable new industrial clusters and advantages to emerge.

For instance, due to the lack of a pipeline, Taiwan’s leading semiconductor firms have proposed more spending in at least three key areas: advanced manufacturing cycles, radio frequency, and quantum. Such increased research spending is particularly urgent in the context of the global productivity slowdown. A recent Organization for Economic Cooperation and Development (OECD) report estimates that between 2001 and 2013, frontier firms experienced productivity growth of 2.8 percent per year compared to just 0.6 percent for others.50 Declining productivity means, in turn, that a proportionate increase of effort will be required just to maintain the status quo level of growth.

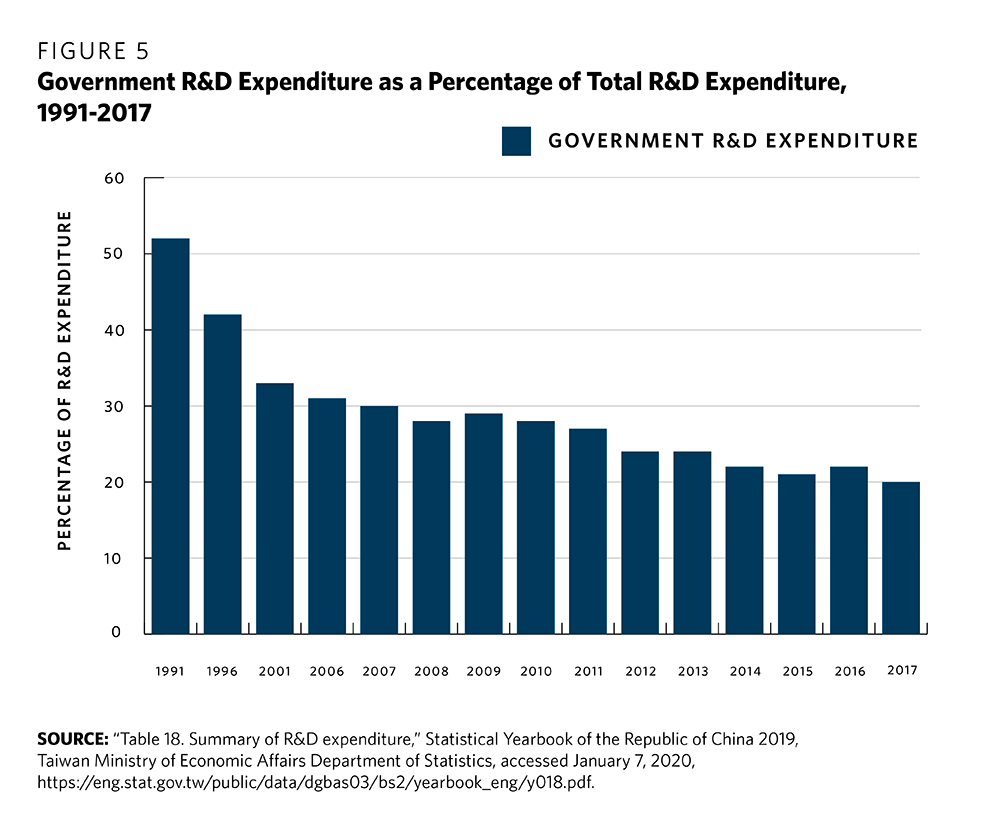

Another study showed that although the United States has managed to sustain its technological progress over many decades, research productivity falls in half every thirteen years, which means that “the economy has to double its research efforts every thirteen years just to maintain the same overall rate of economic growth.”51 In Taiwan, the public sector contribution to total R&D has plummeted from 52.1 percent in 1991 to just 20 percent in 2017 (see figure 5).52

Taiwan’s government can do more through public-private partnerships to encourage commercialization. Many university professors, especially in technical subjects, owe their research sponsorship to the government—for example, through subsidy programs of the Ministry of Science and Technology. But few have been able to respond to government entreaties to commercialize the fruits of this research.53 Fostering links between basic research funding and commercial accelerators and incubators will be essential.

Meanwhile, with political risk rising between Washington and Beijing, Taiwan could be an attractive locale for some of the AI and other laboratories and research partnerships that American and global companies have established in mainland China. Some of these U.S.-Chinese partnerships may erode, or even dissolve, putting Taiwan in a position to potentially pick up the ball if it enhances its own network of partnerships with U.S. corporate and university players over the next three to five years.

Taiwan could also get a boost by continuing to follow international standards and regulatory policy best practices. With competition for foreign investment intensifying, companies will compare policy environments as they weigh where and how to do business around the world. Taiwan’s legal and regulatory requirements can bolster its opportunities if it follows international best practices and advertises itself as a global center of excellence.

For instance, Taiwan has already joined the APEC Cross-Border Privacy Rules system for privacy and data transfer.54 It could continue to uphold its privacy standards and potentially aim to seek an adequacy decision, which is a determination on the basis of Article 45 of EU Regulation 2016/67955 that a party outside the EU offers an adequate level of data protection to meet tests under Europe’s GDPR system.56

The United States, Canada, and Japan are among the very small number of economies to have won such decisions from Brussels. EU talks with South Korea are ongoing. Taiwan should aim to become one of the first few economies in the world to have free data flows with Europe, or else consider some type of privacy and data flows agreement with the United States.

Beyond privacy, Taiwan should also become more active in joining international discussion on technology standards—for instance, by participating in the International Organization for Standardization and International Electrotechnical Commission standards working group on issues like IoT, cyber, and other emerging technologies, where it could help to actively drive the dialogue.57

CONCLUSION

Taiwan has faced strategic and economic obstacles for decades. Yet smart policies, economic heft, and a culture of innovation have helped to make it more secure.

To remain secure for the long term, Taiwan needs to make its economy more robust and to integrate with the broader international environment. Above all, it needs a concerted effort to adapt its economy to rapid industrial and technological change.

One solution is to leverage the harmonization of standards through a U.S.-Taiwan trade agreement, which could include chapters covering trade in both goods and services, as well as e-commerce and investment rules. A stronger trade relationship between the United States and Taiwan would offer a platform to lock in mutually beneficial gains between two APEC partners by negotiating a formal system of shared standards.

To be sure, reaching a free trade agreement (FTA) is rarely a simple endeavor. But for both sides, it offers commercial promise, and for Taiwan it offers a pathway to greater economic security and enhanced international integration.

Still, enhancing trade and investment alone is not enough. An FTA would not, for example, resolve some of the inherent but pressing innovation-related challenges to Taiwan’s economy. And it would hinge heavily on legacy industries, not the emerging fields that are rapidly reshaping the future of work, service delivery, and defense.

Without a reinvigorated innovation ecosystem, Taiwan’s economic prospects will dim. Yet by deploying resources and focusing its educational and innovation strategies in creative ways, Taiwan can adapt to the fresh challenges of this new era. By freeing up access to its talented, well-organized, creative, and educated population, Taiwan will, in time, become a more attractive investment, innovation, and testing hub for a greater variety of international partners.

That is manifestly in Taiwan’s interest. It is precisely why it is so essential to Taiwan’s economic future that it overcome the innovation-related challenges at the heart of this paper.

FUTURE OF TAIWAN’S ECONOMIC COMPETITIVENESS

In 2019, the Asia Program of the Carnegie Endowment for International Peace, in collaboration with the Taiwan WTO & RTA Center of the Chung-Hua Institution for Economic Research (CIER), began to jointly convene a series of roundtables with U.S. and Taiwan stakeholders.

The initiative has two major goals: first, to examine challenges to Taiwan’s future competitiveness and comparative advantage amid technological change, global economic disruption, and rapidly evolving political risk; and second, to explore where and how fresh partnerships between U.S. and Taiwan players can help to bolster Taiwan’s economic future.

The initiative is focused in three areas:

The principal author, Evan A. Feigenbaum (Carnegie Endowment for International Peace), has drawn on collaboration with Roy C. Lee of CIER and especially the extensive insights and contributions of a distinguished group of policy and industry practitioners in both Taiwan and the United States, as well as leading academic and policy analysts.

We particularly acknowledge the detailed comments and critiques on a draft of this paper received from Glenn Gaffney, Alexa Lee, Tim Maurer, AnnaLee Saxenian, and Matt Sheehan.

A very special thank you to Jeremy Smith and Alex Taylor of the Carnegie Endowment for International Peace—for comments on the paper, invaluable background research, and essential support of the project.

https://carnegieendowment.org/2020/01/29/assuring-taiwan-s-innovation-future-pub-80920

EVAN A. FEIGENBAUM

- JANUARY 29, 2020

- PAPER

Summary: Taiwan’s innovation advantage is in danger of eroding. It needs a revitalized and broadened strategy, more diverse investments in human capital and next-generation industries, and forward-looking partnerships with the United States.

Related Media and Tools

Sign up for weekly updates from the Carnegie Endowment for International Peace

If you enjoyed reading this, subscribe for more!

Personal InformationE-mail *E-mail

EXECUTIVE SUMMARY

Innovation has been a source of comparative advantage for Taiwan historically. It has also been an important basis for U.S. firms, investors, and government to support Taiwan’s development while expanding mutually beneficial linkages. Yet, both Taiwan’s innovation advantage and the prospect of jointly developed, technologically disruptive collaborations face challenges.

For one, Taiwan’s technology ecosystem has been hollowed out in recent decades as personal computing (PC), component systems, and mobile device manufacturing moved across the Taiwan Strait to mainland China. Meanwhile, Taiwan’s innovation ecosystem has struggled to foster subsequent generations of startups to replace these losses in electronics manufacturing. Despite a freewheeling startup culture, internationalization has been a persistent challenge for Taiwan-based firms. Technological change and political challenges from Beijing present additional risks to Taiwan’s innovation future.

In this context, it is essential that Taiwan get back to basics if it is to assure its innovation advantage. One piece of this will involve taking a hard look at the domestic policy environment in Taiwan to ensure a steady pipeline of next-generation engineering talent. Yet Taiwan also needs to address several structural and policy factors that, over the last decade, have eroded its enviable innovation advantage.

Evan A. Feigenbaum

Evan A. Feigenbaum is vice president for studies at the Carnegie Endowment for International Peace, where he oversees research in Washington, Beijing and New Delhi on a dynamic region encompassing both East Asia and South Asia.

This paper examines five pressing challenges to Taiwan’s innovation future and proposes an array of specific solutions to promote Taiwan-based innovation, better leverage partnerships with U.S. and other international players, and bolster Taiwan’s standing in the global marketplace.

A particular focus is the need to foster a next generation talent pool with expertise in computer and data sciences, machine learning, and other fields that could contribute to the integration of software with Taiwan’s long-standing comparative advantages in hardware.

Taiwan’s innovation ecosystem has faced particular pressures on its ability to reorient from semiconductor and chipset design and fabrication toward new, future-facing industries. Many of the new systems in these industries do require advanced hardware. But they also require parallel adaptations in software, and the firms and national innovation systems that lead these industries tend to derive their competitive advantages from hardware-software integration.

To this end, forward-looking partnerships between Taiwan and U.S. players could naturally complement a revitalized and broadened innovation strategy for Taiwan.

INTRODUCTION

Innovation has been a source of comparative advantage for Taiwan historically. It has also been an important basis for U.S. firms, investors, and government to support Taiwan’s development while expanding mutually beneficial linkages.

But both of these things—Taiwan’s innovation advantage and the prospect of jointly developed, technologically disruptive collaborations—face challenges.

In the 1980s and 1990s, mutually beneficial collaborations between Silicon Valley and the broader Hsinchu-Taipei region supported entrepreneurial dynamics and the growth of the indigenous semiconductor and PC industries in Taiwan. In the 2000s, however, Taiwan’s technology ecosystem hollowed out as PC, component systems, and mobile device manufacturing moved across the Taiwan Strait to mainland China. Today, the Ministry of Economic Affairs (MOEA) annual survey has shown that over 80 percent of Taiwan’s information and communication technology (ICT)–related products are manufactured in China.1

Bluntly put, Taiwan’s innovation ecosystem has struggled to foster subsequent generations of startups to replace these losses in electronics manufacturing—for instance, in software, computer security, data, chips, and artificial intelligence.

But that is not all. Despite a freewheeling startup culture, internationalization has been a persistent challenge for Taiwan-based firms. A 2018 report from the Chung-Hua Institution for Economic Research concluded that while Taiwan’s total research and development (R&D) investment accounted for 3.05 percent of gross domestic product (GDP) in 2015, just 0.06 percent of private sector R&D activities are funded by foreign sources.2 Similarly, a 2018 PWC survey of Taiwan’s startup ecosystem revealed a significant lack of internationalization, with 71 percent of revenue sources for Taiwan-based startups generated by the comparatively small domestic market.3 Successful Taiwan startups with ambitions to expand overseas were revealed in this survey to lack the resources to do so.

This is just one of many areas that revitalized and strengthened partnerships between Taiwan and U.S. players could help to address. Taiwan-based startups appear keen to attract external investment, not just to obtain capital but also to plug into global networks.

Meanwhile, technological change and political challenges from Beijing present additional risks to Taiwan’s innovation future.

For one, Chinese state policies have thus far precluded Taiwan from forging industrial and commercial links in the context of formal investment, trade, or other framework agreements with regional governments, especially in the Southeast Asian countries that are critical parts of the East Asian manufacturing supply chain.

For another, the bleeding of talent across the Taiwan Strait has been a persistent challenge to Taiwan-based industry. Since 2017, Beijing has sought to ramp up its own domestic semiconductor industry, in part by poaching Taiwan-based talent.4 One recent report suggests that as many as 3,000 semiconductor engineers have departed Taiwan for positions at Chinese companies, a figure that would amount to nearly one-tenth of Taiwan's roughly 40,000 engineers involved in semiconductor R&D.5