Challenge to India and Africa: Premature Deindustrialization

One of the biggest challenges facing the developed world is static population growth. Japan’s population is actually decreasing. China too, despite its 1.3 billion people, is bracing for a population crisis as it reaps the consequences of its notorious “one family one child” policy. In China, Japan, Europe and the U.S. dwindling populations of workers will be required to support mushrooming populations of retired elderly. Fewer people also means fewer households being formed. The developed world is struggling to grow amid declining consumer demand.

But the picture may be even worse where population growth is robust. India is expected to surpass China in population by 2022, and have 1.7 billion people by 2050. India adds a million working age people each month. Population growth is even more impressive in Africa where the population is expected to double by 2050 to 2.5 billion people. There will be almost 400 million Nigerians by then, making it more populous than the U.S.

Theoretically, India and Africa could serve as growth engines for the world as all of those people creating new households provide almost unlimited consumer demand. But for consumer demand to flourish there must be a strong economy endowing consumers with spending power. History teaches that a strong economy begins with a viable manufacturing base.

Unfortunately, in both India and Africa strong manufacturing sectors are struggling to be born. Harvard economist Dani Rodrik sees what he called “premature deindustrialization” as manufacturing shrinks in poor countries that never industrialized much in the first place. India with its armies of low wage workers could have gone on a manufacturing binge like China, but its manufacturing output is actually declining as a percentage of the economy. The story is the same in Africa. In South Africa, for example, manufacturing was 15 percent of output in 1962, peaked at 25 percent in 1981, but by 2011 was down to 18 percent.

There are many obvious reasons for the failure of manufacturing to lift off in India and Africa. The first and most obvious is that manufacturing needs a solid infrastructure to enable efficient transfer of raw materials and shipment of finished goods to market. The roads, rails, ports and air service in India and Africa are woefully inadequate. We think our infrastructure is bad, and for sure it needs more investment, but it is light years ahead of India and Africa.

For manufacturing to flourish, there must be effective government. India has democracy but too often that enables citizens to block needed modernization of infrastructure. With a few exceptions, the governments of Africa are conspicuously inept. Africa’s abundant resources somehow never benefit the people or provide capital for industrial development. In Nigeria, which should be a rich country, only 9 percent of adults are employed full time by someone else.

India and Africa, like the rest of the world, are today flooded with low cost manufactured goods made in China and other Asian nations, and with the advent of the robot age the value of unskilled labor is declining everywhere. Now India and Africa must find a viable path to prosperity without passing through an industrialization phase. This is not likely to happen. It is by no means clear that it is even possible.

Jerry Jasinowski, an economist and author, served as President of the National Association of Manufacturers for 14 years and later The Manufacturing Institute. Jerry is available for speaking engagements. December 2015

India Must Reverse Its Deindustrialization | PIIE

Can India be a manufacturing powerhouse? Three developments make that question salient today. Looming ahead is the demographic bulge, which will disgorge a million young people every month into the economy in search of employment opportunities. Rising labor costs in China create opportunities for low-skilled countries such as India as replacement destinations for investment that is leaving China. And a new government assuming power later this month offers the prospect of refashioning India in the image of Gujarat, which has been one of the few manufacturing successes.

Manufacturing is an important sector into which resources should flow for two reasons: the level of productivity and its dynamism. If this were to happen, the economy would become more productive through a reallocation of resources from less productive to more productive sectors and also because productive sectors would become more so over time.

In India, the sector with these characteristics is registered (formal) manufacturing. According to our calculations, the level of labor productivity (measured as value added divided by employment) in 2010 was about 4.2 times greater in formal manufacturing than in the rest of the economy. Second, between 1999 and 2010, productivity in this sector grew at an annual average rate of 5.3 percent compared with 4.3 percent for the rest of the economy. Note that these benefits only pertain to formal manufacturing because informal manufacturing is a low-productivity and non-dynamic sector—compared to not just formal manufacturing but large parts of the economy.

Thus, the desirability of India becoming the next China or the next Gujarat is not in doubt. The real issue, and the open question, relates to feasibility. And there is a sobering fact here: India has been deindustrializing, big time.

In a piece that one of us wrote recently, we noted the fact, first pointed out by Dani Rodrik, that "early" or "premature" deindustrialization is happening worldwide. At any given stage of development, countries are on average specializing less in manufacturing. Furthermore, the point in time at which the share of industry peaks (alternatively, the point at which deindustrialization begins) is happening earlier in the development process.

For example, in 1988, for the world as a whole, the peak share of manufacturing in gross domestic product (GDP) was 30.5 percent on average and attained at a per capita GDP level of $21,700. By 2010, the peak share of manufacturing was 21 percent (a drop of nearly a third) and attained at a level of $12,200 (a drop of nearly 45 percent).

What has been the equivalent development within the Indian states? The table provides data, showing the year in which the share of registered manufacturing in GDP peaked, the peak level of manufacturing, and the per capita GDP associated with peak manufacturing levels.

A few points are striking. Gujarat has been the only state in which registered manufacturing as a share of GDP surpassed 20 percent and came anywhere close to levels achieved by the major manufacturing successes in East Asia. Even in Maharashtra and Tamil Nadu, manufacturing at its peak accounted for only about 18 to 19 percent of state GDP.

Second, in nearly all states (with the possible exception of Himachal Pradesh), manufacturing is now declining and has been doing so for a long time. The peak share of manufacturing in many states was reached in the 1990s (Gujarat and Tamil Nadu) or even in the 1980s (Maharashtra).

Third, and this is perhaps the most sobering of facts, manufacturing has even been declining in the poorer states: States that never effectively industrialized (West Bengal, Uttar Pradesh, and Rajasthan) have started deindustrializing.

Some comparisons are illuminating. Take India's largest state, Uttar Pradesh. It reached its peak share of manufacturing, of 10 percent of GDP, in 1996 at a per capita state domestic product of about $1,200 (measured in 2011 purchasing power parity dollars). Indonesia attained a manufacturing peak share of 29 percent and at a per capita GDP of $5,800. Brazil attained its peak share of 31 percent at a per capita GDP of $7,100. So, Uttar Pradesh's maximum level of industrialization was about one-third that in Brazil and Indonesia; and the decline began at 15 to 20 percent of the income levels of these countries.

These findings serve to emphasize that if India is to become a manufacturing powerhouse, it has to reverse a process that has been entrenched for several years in several states. It is not that patterns of specialization cannot be changed. But that reversal will require a lot of hard work, so that a critical mass of policies is changed to create an environment that is conducive to making high-productivity manufacturing attractive to investment, domestic and foreign.

Time, or rather the weight of history, is not on the side of Indian manufacturing.

Arrested development

THIRTY-FIVE YEARS ago Shenzhen was a tiny fishing village just over the river from British Hong Kong. Its inhabitants, like most Chinese, lived in poverty. In 1978 the average income in America was about 21 times that in China. But in 1979 China’s leader, Deng Xiaoping, chose Shenzhen as the country’s first special economic zone, free to experiment with market activity and trade with the outside world. Shenzhen quickly found itself at the leading edge of Chinese economic development, using the same model as Japan, South Korea and Hong Kong itself had done at earlier stages. In the late 1970s China was bursting with cheap, unskilled labour. It opened its doors (a crack, in lucky places like Shenzhen) to foreign manufacturers waiting to take advantage of these low labour costs. Even though wages were at rock bottom, both productivity and pay in urban factories were dramatically higher than in agriculture, so China’s fledgling industrialisation attracted a steady flow of migrants from the countryside.

Over time local production became more sophisticated and wages went up. Industrial cities served as escalators for development, linking the Chinese economy with global markets and allowing incomes to rise steadily. The fruits of this process are clearly visible. As visitors approach the checkpoints between Hong Kong and the mainland, a modern skyline rises on the horizon. Great glass-sheathed skyscrapers reach upwards in central Shenzhen, which boasts some of the world’s tallest buildings. At street level Chinese workers stroll past shopfronts displaying Western luxury brands: Ferrari, Bulgari, Louis Vuitton.

Governments across the emerging world dream of repeating China’s success, but the technological transformation now under way appears to be permanently changing the economics of development. China may be among the last economies to be able to ride industrialisation to middle-income status. Much of the emerging world is facing a problem that Dani Rodrik, of the Institute for Advanced Study in Princeton, New Jersey, calls “premature deindustrialisation”.

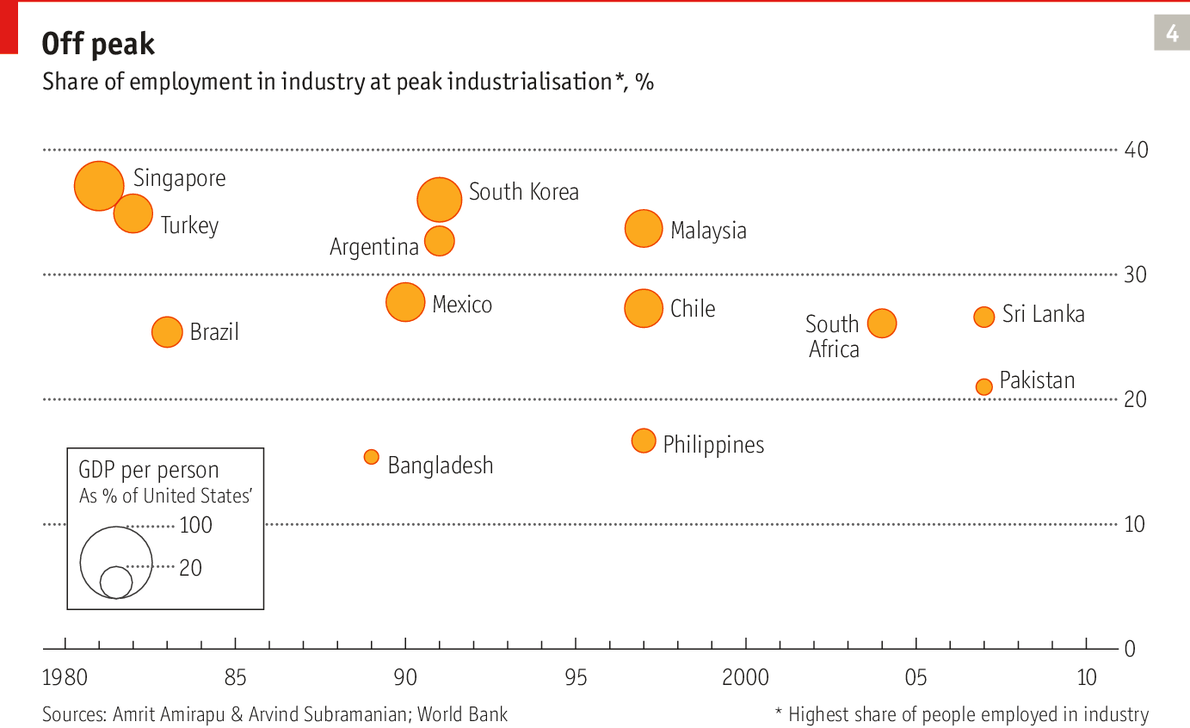

For most of recent economic history, “industrialised” meant rich. And indeed most countries that were highly industrialised were rich, and were rich because they were industrialised. Yet this relationship has broken down. Arvind Subramanian, of the Peterson Institute for International Economics and reportedly soon to become chief economic adviser to the Indian government, notes that, at any given level of income, countries today are less reliant on manufacturing, in terms of both output and employment, than they were in the past, and that the level of income per person at which reliance on manufacturing peaks has also declined steadily (see chart 4). When South Korea reached that point in 1988, its workers’ earnings averaged just over $10,000 (in PPP-adjusted 2011 dollars) per person. When Indonesia got there in 2002, average income was just under $6,000, and for India in 2008 it was just over $3,000.

Premature non-industrialisation

Early loss of industry (or, in India’s case, what Mr Subramanian calls “premature non-industrialisation”) is a distressing trend, given the role that exports of goods have historically played in economic development. Productivity in export industries is generally high, otherwise they could not compete in global markets. Over time, productivity in making traded goods tends to rise as firms and workers in the industry become familiar with the technologies involved. Past developmental success stories such as the Asian tigers moved from low-margin, labour-intensive goods such as clothing and toys to electronics assembly, then on to component manufacture and, in the textbook cases of Japan and South Korea, to advanced manufacturing, design and management.

Export success trickles down to the rest of developing economies. Since producers of non-traded goods and services, such as housebuilders and lawyers, must compete with exporters for labour, they need to pay attractive wages. At the same time the chance of well-paid work in manufacturing creates an incentive for workers to move to cities and invest in education. An industrialising export sector is like a speedboat that pulls the rest of the economy out of poverty.

Loss of industry at low income levels, by contrast, caps the contribution that manufacturing can make to domestic living standards. That is no small problem: there is no obvious alternative strategy for turning poor countries into rich ones.

The change in technology’s role in development began in the 1980s. Richard Baldwin, an economist at the Graduate Institute of International and Development Studies in Geneva, explains that for much of modern economic history the driving force behind globalisation was the falling cost of transport. Powered shipping in the 19th century and containerisation in the 20th brought down freight charges, in effect shrinking the world. Yet since the 1980s, he says, cheap and powerful ICT has played a bigger role, allowing firms to co-ordinate production across great distances and national borders. Manufacturing “unbundled” as supply chains scattered across the world.

According to Mr Baldwin, this meant a profound change in what it is to be industrialised. The development of an industrial base in Japan and South Korea was a long and arduous process in which each economy needed to build capabilities along the whole of a supply chain to manufacture finished goods. That meant few economies managed the trick, but those that did were rewarded with a rich and diverse economy.

In the era of supply-chain trade, by contrast, industrialisation means little more than opening labour markets to global manufacturers. Countries that can grab pieces of global supply chains are quickly rewarded with lots of manufacturing employment. But development that is easy-come may also be easy-go. Unless the economies concerned quickly build up their workers’ skills and infrastructure, wage increases will soon lead manufacturers to up sticks for cheaper locations.

From stuff to fluff

Another mechanism through which new technology is changing the process of development is the dematerialisation of economic activity. Consumption the world over is shifting from “stuff to fluff”, reckons Mr Subramanian. People everywhere are spending a larger share of their income on services such as health care, education and telecommunications. This shift is reflected in trade. Messrs Subramanian and Kessler note that, measured in gross terms, goods shipments dominate trade as much as ever. They accounted for 80% of world exports in 2008 (the most recent figure available), down only slightly from 83% in 1980. Measured in value-added terms, however, the importance of goods trade tumbled, from 71% of world exports in 1980 to just 57% in 2008, because of the increasing weight of services in the production of traded goods. Much of the value of an iPhone, for example, derives from the original design and engineering of the product rather than from its components and assembly.

A recent report by the McKinsey Global Institute put the value in 2012 of “knowledge-intensive” trade—meaning flows of goods or services in which research and development or skilled labour contribute a large share of value—at $12.6 trillion, or nearly half the total value of trade in goods, services and finance. Physical assembly accounts for a declining share of the value of finished goods. The knowledge-intensive component of trade is also growing more quickly than trade in labour-, capital- or resource-intensive products and services. At the same time the dramatic decline in the cost of information and communications technologies has opened up trade in some high-value services. Skilled programmers in India, for example, can sell IT services around the world despite the low overall level of development of the Indian economy.

India has masses of cheap, unskilled labour that ought to be attractive to firms wanting to set up low-cost manufacturing facilities. Yet operating them would require at least some skilled workers, and the rising premium on these created by trade in ICT services makes it uneconomic for many would-be manufacturers to hire the necessary talent. Mr Subramanian and Raghuram Rajan, another Indian economist, have dubbed this the “Bangalore bug”, a reference to the extraordinarily successful ICT cluster in the southern Indian city of Bangalore. But other emerging economies are similarly affected.

Other advances are eliminating the need for human labour altogether. Walking through an electronics production line at Foxconn’s Longhua campus in Shenzhen, a worker points out places where people have already been replaced by machinery—“to reduce injuries to workers”, he says. Elsewhere on the line he indicates a place where a robot is being tested to take over a range of tasks from humans. Perhaps 10% of the staff at Longhua now consists of engineers working on such automation.

Successful solutions will be rolled out to other Foxconn facilities, says Louis Woo, a special adviser to Foxconn’s chairman, Terry Gou. And Foxconn has even greater ambitions. In Chengdu it is working on a “lights out”, entirely automated, facility which serves a single, as yet unnamed, customer. In fast-developing and rapidly ageing China workers are becoming increasingly expensive, as well as hard to find. Automation provides a means to hold on to work that might otherwise pack up and move to another country.

It also saves a lot of trouble. Vast areas of Foxconn’s Longhua campus are given over to support services for the roughly quarter of a million workers employed there: shops and restaurants, a massive central kitchen with automated rice-cooking equipment, dormitories that house about half the staff, schools for workers’ children and counselling services for distressed employees. Foxconn’s dormitories are ringed with netting, a precaution prompted by an epidemic of suicides by workers that set off a torrent of bad press for the company and its customers. Indeed, notes Mr Woo, it is often customers that are behind the push for greater automation of Foxconn’s facilities.

The falling cost of automation makes the use of robots attractive even in India, where cities are swarming with underemployed young workers. The main reason for that is the country’s thicket of red tape. Mr Subramanian thinks India’s best hope now may be to concentrate on churning out more highly skilled workers, rather than count on manufacturing to mop up its jobless millions.

The rapid growth in emerging economies over the past 15 years was good for many very poor countries in Africa and Central America, but most still grew more slowly than richer developing countries in Asia and South America. Given the institutional weakness, inadequate infrastructure and modest skills base in many of the world’s poorest places, even rock-bottom wages there may be insufficient to attract much manufacturing.

That is a distressing prospect. The United Nations estimates that sub-Saharan Africa’s population will roughly triple over the next half-century, to about 2.7 billion. A development model in which rapidly rising incomes are limited to a highly skilled few is unlikely to be sustainable. Many talented workers are already thinking about emigrating, yet rich economies trapped by growing social spending and shrinking tax bases are more likely to slam their borders shut. Over the past decade or two inequality, despite rising within many economies, has shrunk at the global level, thanks to rapid growth in large emerging markets. But in the absence of a new development model, that happy state of affairs may soon be reversed.